Social Market Analytics has been creating security level sentiment metrics for six years. As we build an out-of-sample history we are able to build longer holding period indexes. I have blogged about longer term factors before, this is the most comprehensive portfolio strategy built using sentiment level data. This blog will discuss the application of sentiment to a long only 50 stock, re balanced annually, index.

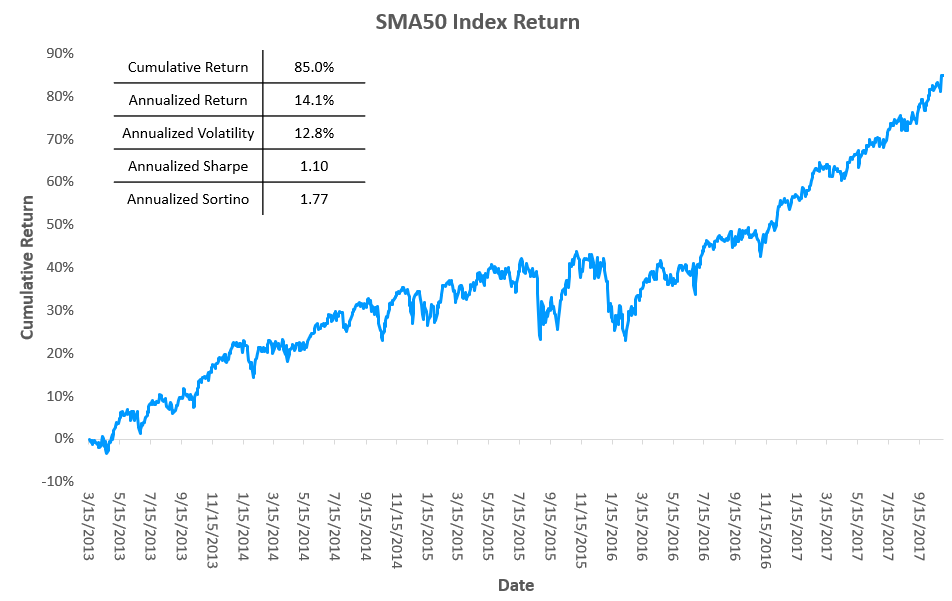

SMA50 Index is a new, capitalization weighted index comprised of 50 stocks with these features:

- The highest average unique message source counts, from SMA’s filtered Twitter data stream, observed over a 50-day look back interval, and

- High daily average dollar trading volume (ADV), > $20 Mil, over a 50-day look back interval. We are looking for liquid stocks.

The SMA50 index measures the aggregate performance of stocks with high levels of crowd sourced commentary and high market liquidity.

- SMA50 is reconstituted each year on March 15th. The core constituents are selected once a year. They are re-weighted monthly based on the below tilt methodologies.

- SMA50 is the “Parent Index” for SMA50 Factor Tilt Products

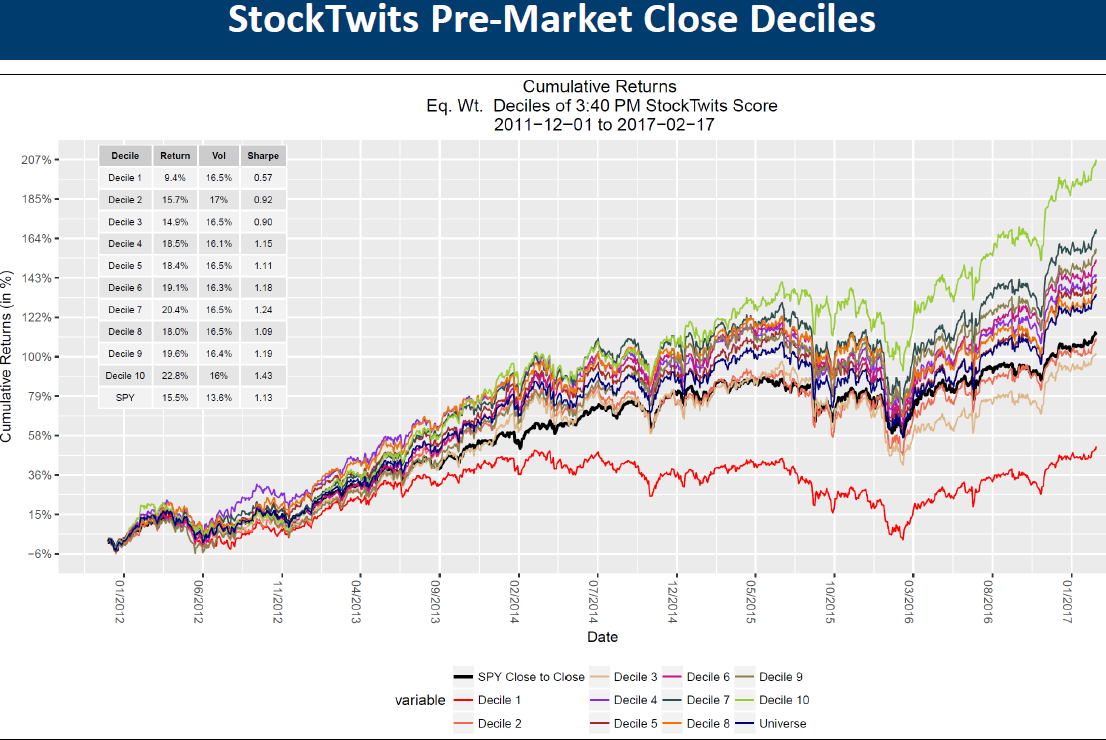

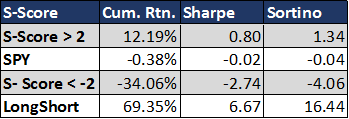

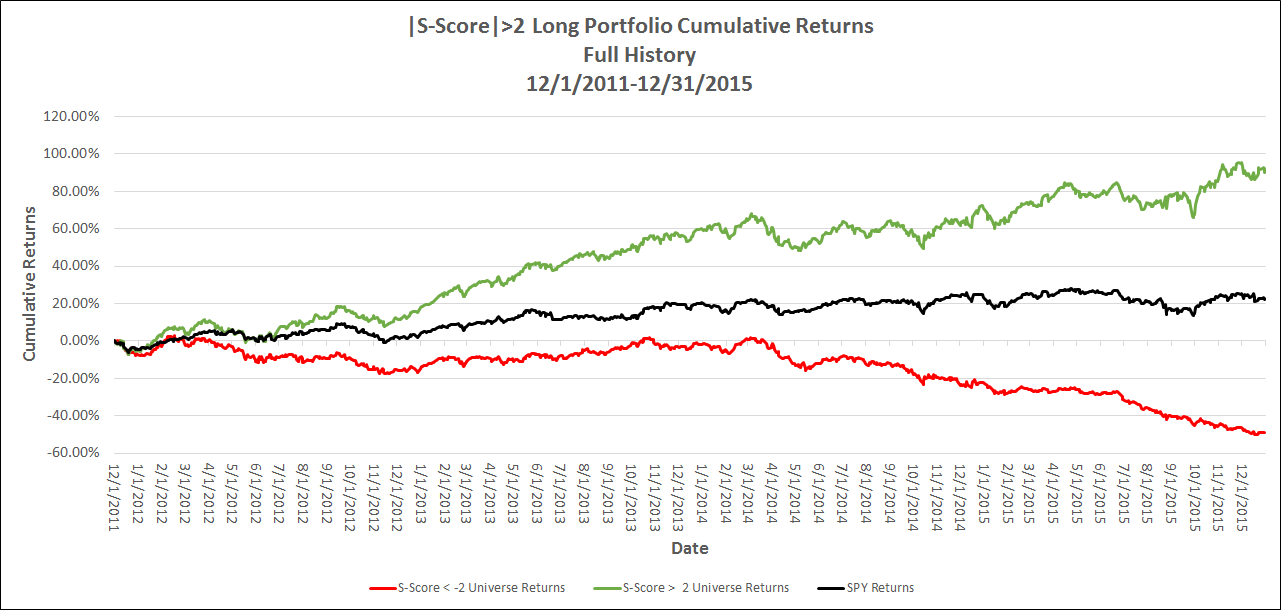

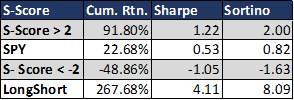

Below is the historical performance of the SMA50 Index. We will add tilting to the index based on sentiment and momentum.

The following factor tilt indexes are derived from the equity universe of the SMA50 parent index. Factor Tilt Indexes are re-balanced monthly on the first market day of the month.

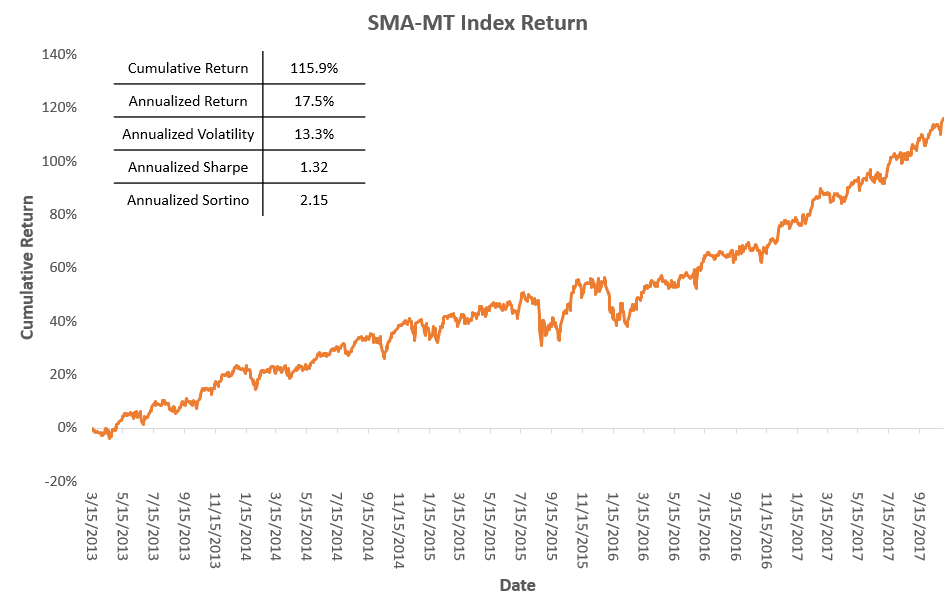

SMA-MT: Momentum Tilt

– Designed to deliver the performance of an equity momentum strategy by emphasizing stocks with high risk-adjusted price momentum.

- A momentum value is determined for each stock in the SMA50 parent index Universe by combining the stock’s recent 12-month and 6-month price performance. This is the standard implementation of a price momentum value.

- This momentum value is then risk-adjusted to determine the stock’s Momentum Score.

- All securities in the SMA50 Universe are weighted by the product of their Momentum Score and their market cap, as follow:

Momentum Weight for SMA-MT = Momentum Score * Market Capitalization Weight in the SMA50. Momentum weights are normalized to sum to 100%.

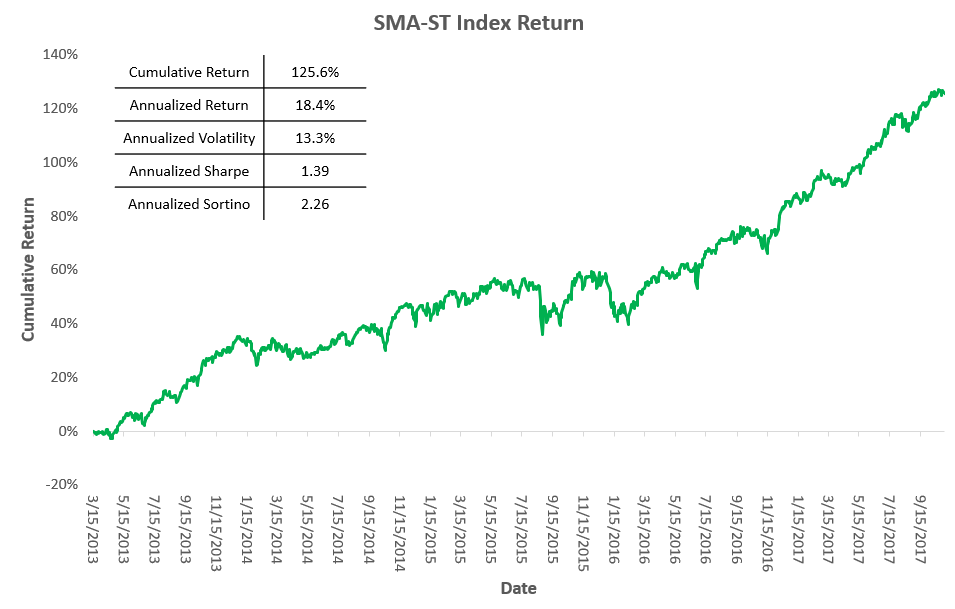

SMA-ST: Sentiment Tilt

– Using SMA’s S-Score and SV-Score as factors, emphasize stocks with positive levels of social media sentiment and intensity, while attenuating stocks with low sentiment levels.

- A composite factor score is determined for each stock in the SMA50 parent index Universe from the linear combination of the stock’s monthly S-Score and monthly SV-Score.

- This composite factor score is used to determine the stock’s Sentiment Score.

- All securities in the SMA50 Universe are weighted by the product of their Sentiment Score and their market cap, as follow:

Sentiment Weight for SMA-ST = Sentiment Score * Market Capitalization Weight in the SMA-50. Sentiment weights are normalized to sum to 100%.

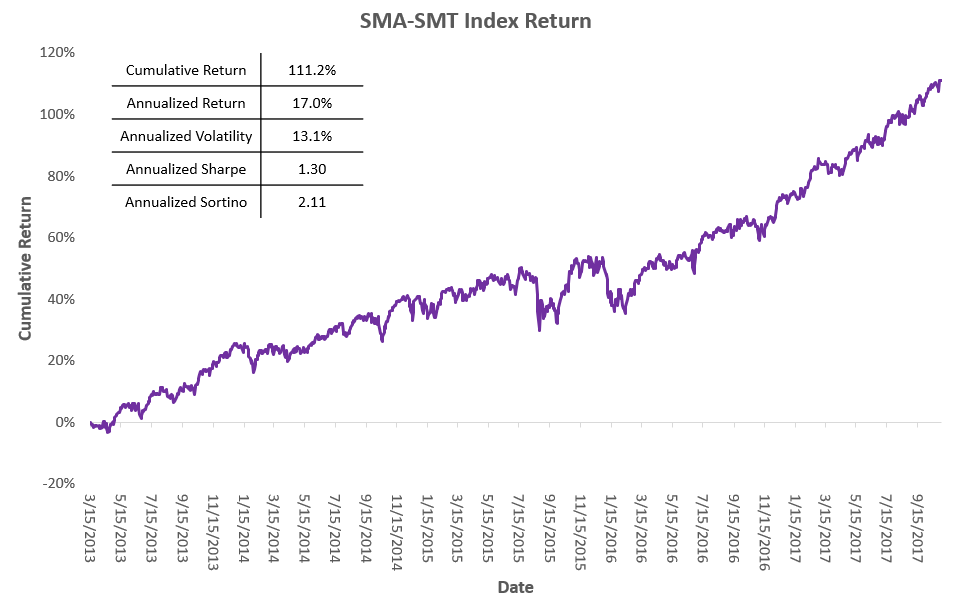

SMA-SMT: Blended Tilt

–Define a factor which is a combination of sentiment and momentum tilts.

- A combined factor is determined for each stock in the SMA50 parent index Universe from a linear combination of the stock’s Momentum and Sentiment scores. Initial results for the blended tilt factor used an equal weighting of Momentum and Sentiment scores.

- This combine factor score is then standardized and used to determine the stock’s Senti-Momentum Score.

- All securities in the SMA50 Universe are weighted by the product of their Senti-Momentum Score and their market cap, as follow:

Senti-Momentum Weight for SMA-SMT = Senti-Momentum Score * Market Capitalization Weight in the SMA-50. Senti-Momentum weights are normalized to sum to 100%.

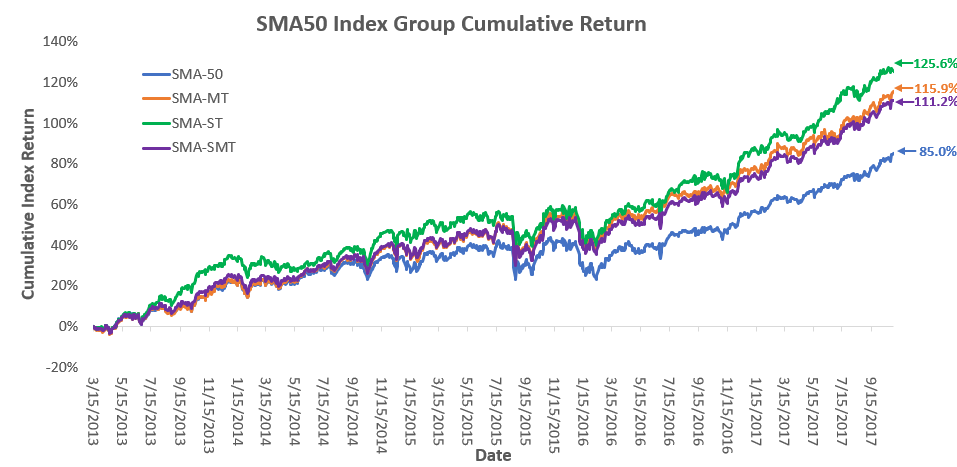

Comparative performance for all four theoretical portfolios is below.

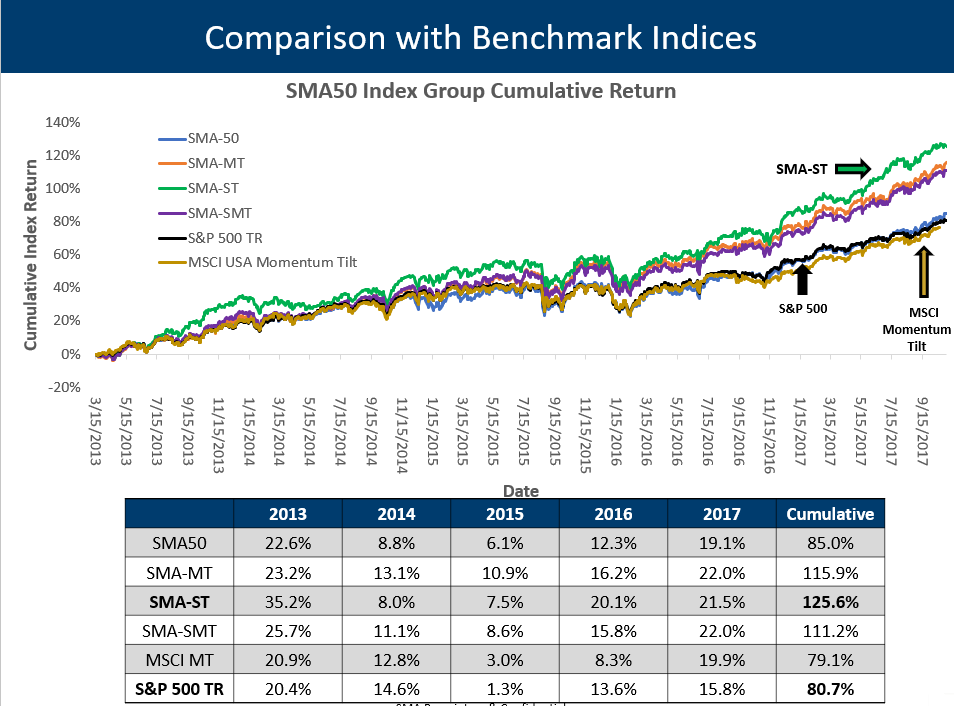

Overlaying standard benchmark performance you can clearly see the effectiveness of the SMA 50 with various tilt strategies to outperform the benchmarks.

The SMA 50 family of indexes provide a low turnover way to benefit from exposure to social sentiment. To learn more please contact us at ContactUs@SocialMarketAnalytics.com