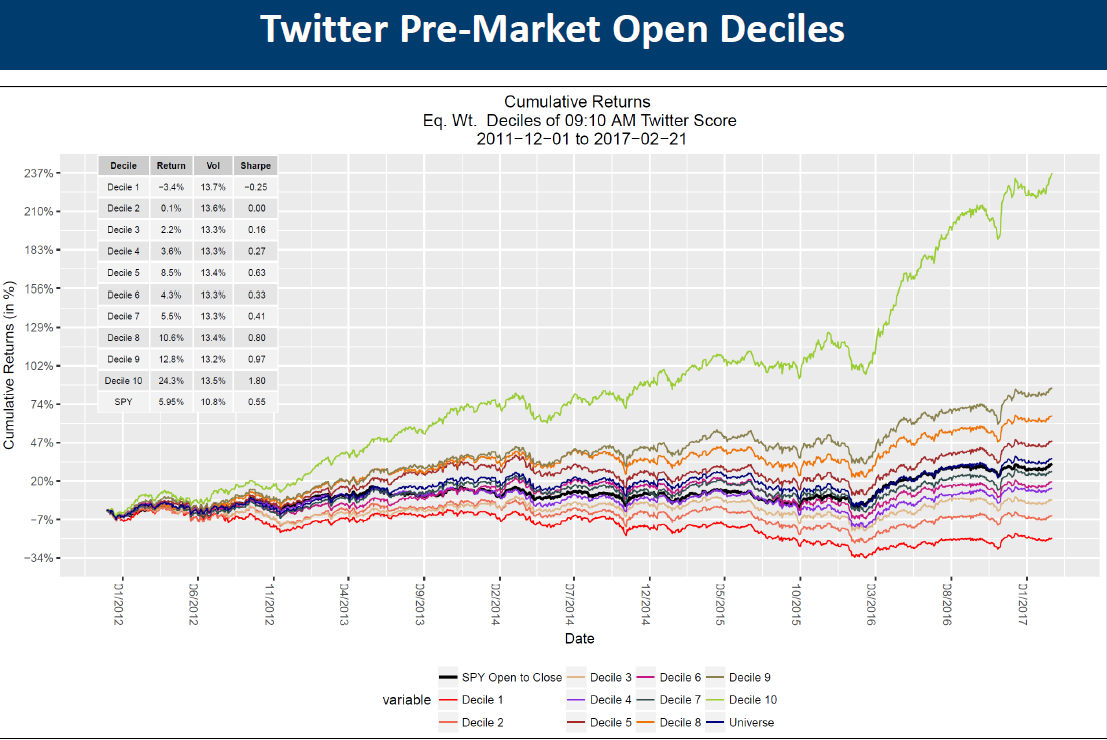

Today I will explore decile groupings based on S-Scores, and plot cumulative subsequent returns. We typically focus on an S-Score > 2 for subsequent positive movements in stock prices, and an S-Score < -2 for negative movements in stock price.

Our metrics identify when a conversation becomes significantly more positive or negative than normal. Most stocks have normal conversations on any given day. On these days there are other factors driving the security. “Normal” conversation securities will typically follow the market, as you see in the SMA data set. High sentiment out-performs and low sentiment under-performs, Open to Close, and Close to Close, across Twitter and StockTwits.

The only filter we add is that the prior day’s closing price must be above $5, to avoid penny stocks. Total return time series are used for returns, and time series are equal weighted.

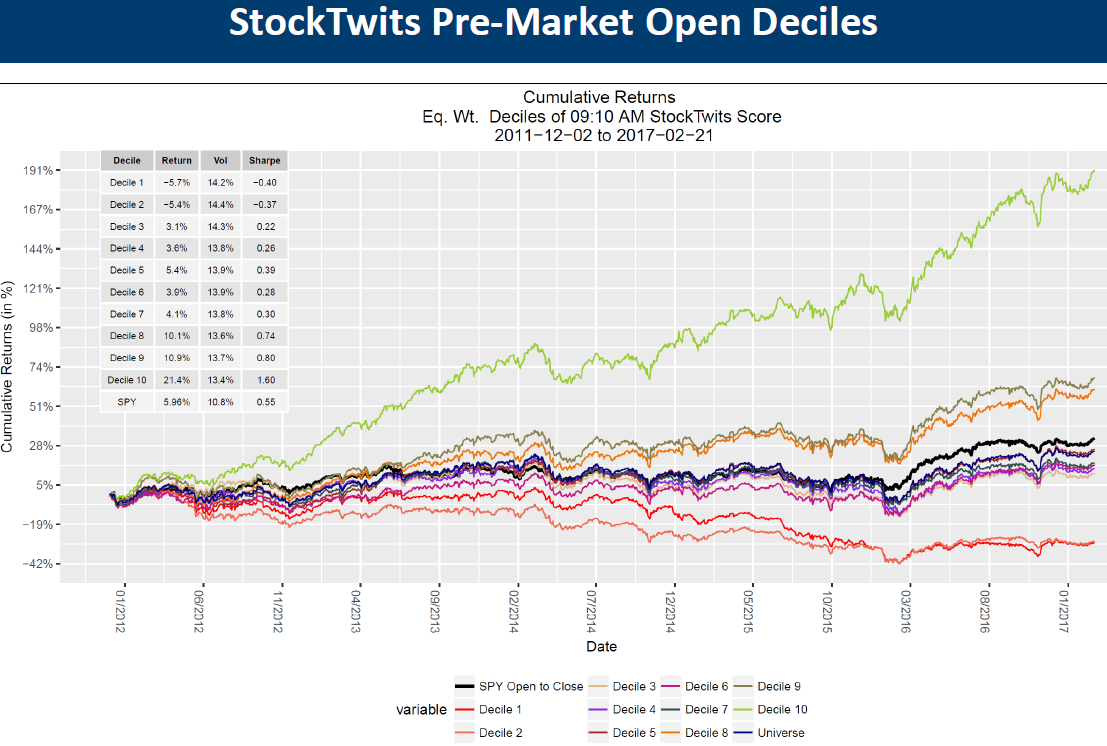

The first chart illustrates subsequent Open to Close returns based on S-Score deciles at 9:10 a.m. Eastern time. As you can see, the deciles are in order with top decile securities out-performing and bottom decile securities under-performing. SPY is represented by the black line and the universe is blue.

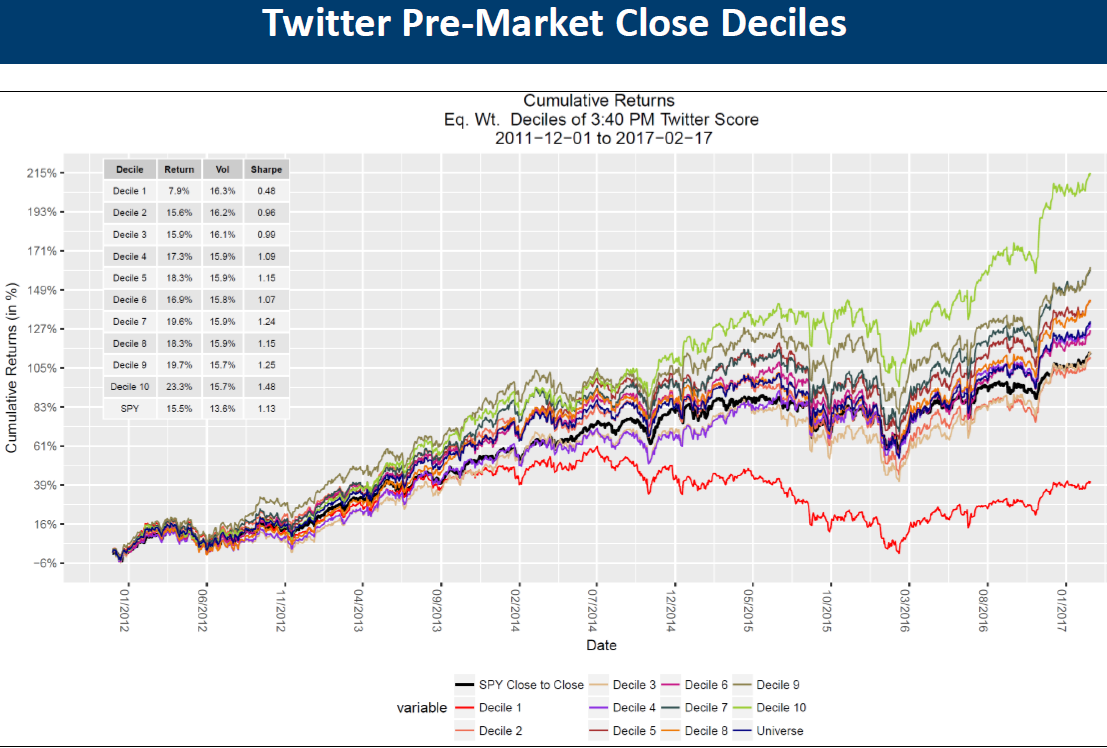

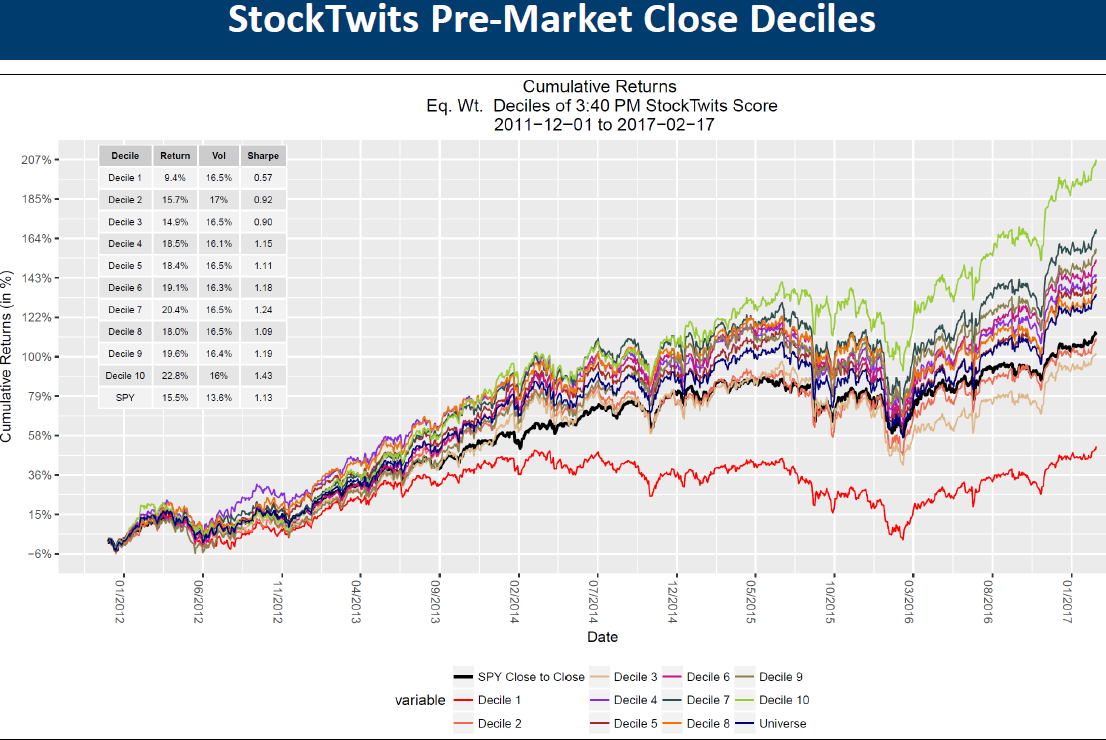

Pre-Market Close deciles are below. S-Scores are taken at 3:40 p.m. Eastern and Close to Close returns are calculated. Again, high S-Score securities out-perform and low S-Score securities under-perform, with the universe in the middle.

StockTwits is the largest chat community for active traders. Its users are professional traders discussing long and short positions. The below chart looks at S-Score decile returns based on StockTwits conversations.

Data is consistent across deciles. A unique characteristic of the StockTwits feed is that there are significant short conversations. The lowest two deciles have negative returns. This is a function of the StockTwits community being able to short securities by direct short selling or taking net short options positions.

Pre-market close deciles are below.

To learn more about Social Market Analytics and the products we offer please visit our website, or contact us here.

Thanks,

Joe