In this video we explain how our S-Factor feed uses the Twitter firehose to build trading signals, dashboards and widgets to help investors increase alpha. To find out how SMA can help your firm, email us at ContactUs@SocialMarketAnalytics.com or schedule a meeting using our 1 on 1 Meeting Signup.

Posts

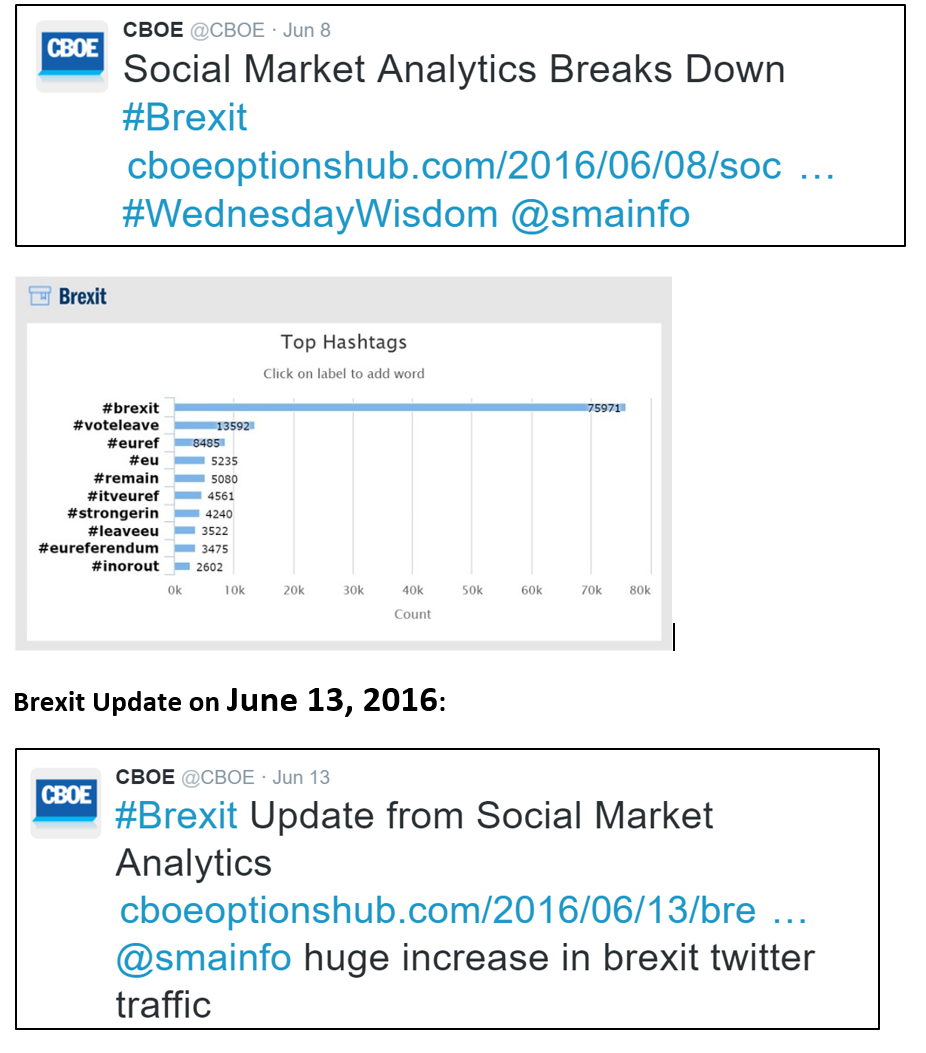

People seem surprised that Britain voted to exit the EU. We at SMA with our partners the CBOE are not nearly as surprised as everyone else. Russell Rhoads from the CBOE has been blogging and Tweeting with SMA data for two weeks that it looks like the Brexit is going to happen. Let’s look at the timeline. Again, this is not a post analysis, these Tweets were out there 2 weeks ago!

Brexit Post on June 8, 2016:

Russell Rhoads, from CBOE wrote a blog about Brexit using the using SSE, the results indicated that an Exit is going to be the result of the vote.

The update from our partners at CBOE talked about the huge increase in Twitter volume about #brexit. One of the key observations was the #VoteLeave campaign had gained far more popularity than the remain campaign. To everyone who was looking, Twitter had shown the signs of a British Exit.

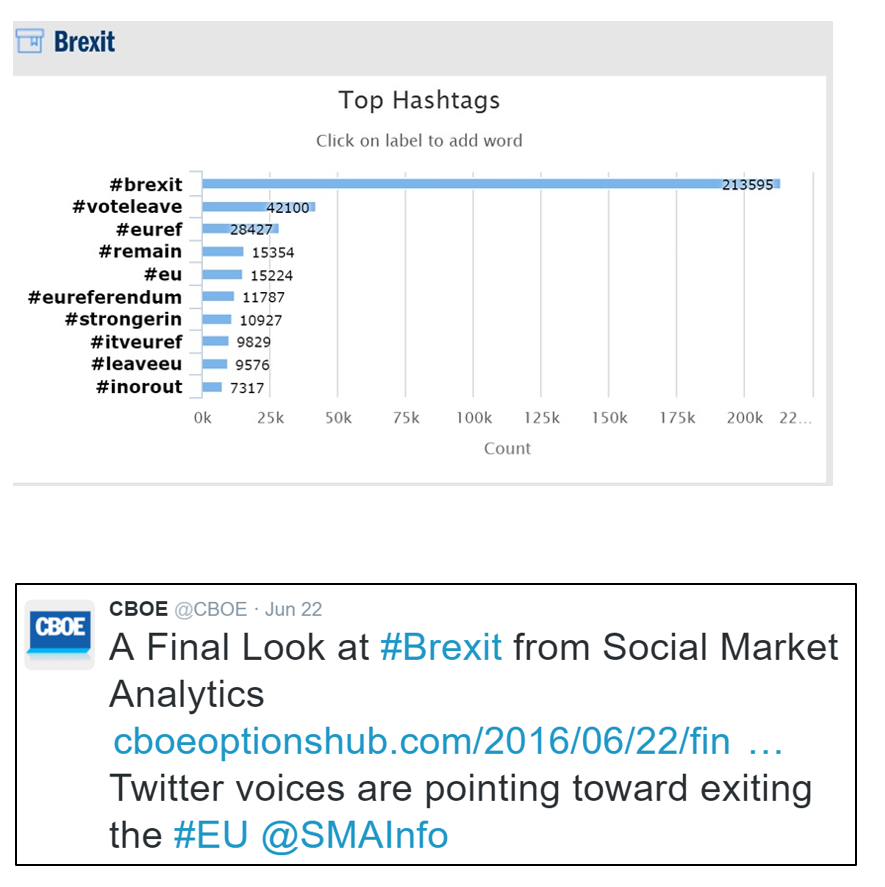

The final post on June 22 talked about strong social media indicators towards the exit. The #VoteLeave campaign has dwarfed the conversations of every other opinion, including the BBC debate. The prediction turned out to be true.

Twitter is the premier leading source of information and SMA can help you make sense of it. Please contact SMA for more information at contactus@socialmarketanalytics.com

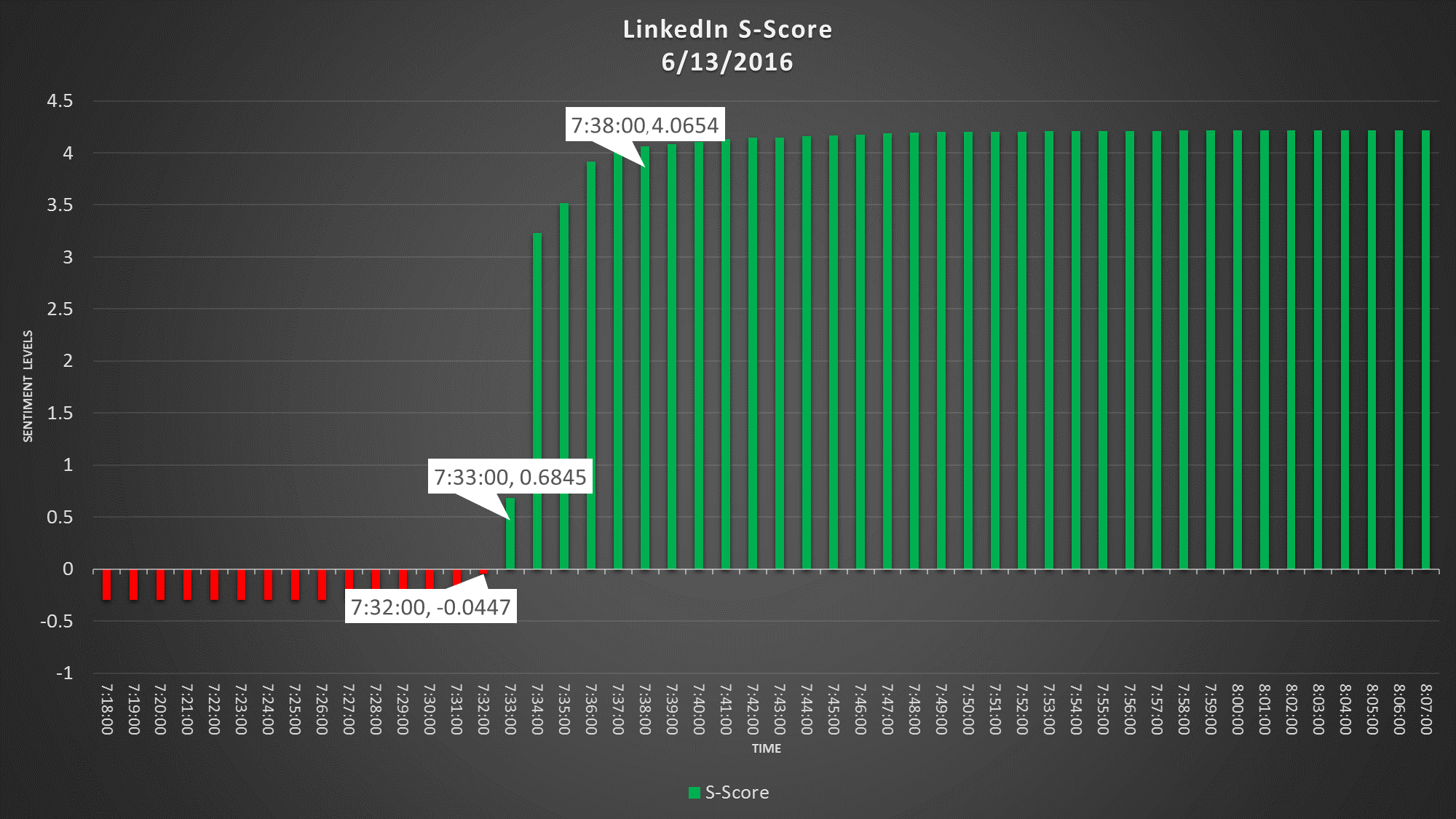

As is the case with most corporate events now, MSFT buying LNKD broke on Twitter first. The very first mention of this is any news article was at 7:38 AM (CDT) but Social Market Analytics (SMA) detected this 7 minutes ahead at 7:31. SMA’s patented algorithm digests, filters and evaluates Tweets in real time. The filtering process, a proprietary Tweet account filtering technology built by SMA, separates signal from noise by continuously scanning for accounts that are deemed credible to be included in the calculation process. The tweets from spam accounts are filtered right away.

The following are the 5 tweets that SMA received from these credible accounts in a matter of 13 seconds. All of them pointing towards the same positive news.

The 7:32 AM sentiment, as a result, had already started moving positive. By the next minute, at 7:33 AM the sentiment was already positive and soaring up. By the time other news sources caught up to this news, at 7:38 AM, the sentiment was already very positive. The S-DeltaTM alerts which measures the 15 minute changes in the sentiment had started firing up at 7:33 AM as people took notice of this and the Tweet volume kept soaring.

Contact SMA for more information about using Twitter based metrics in your investment process: info@SocialMarketAnalytics.com

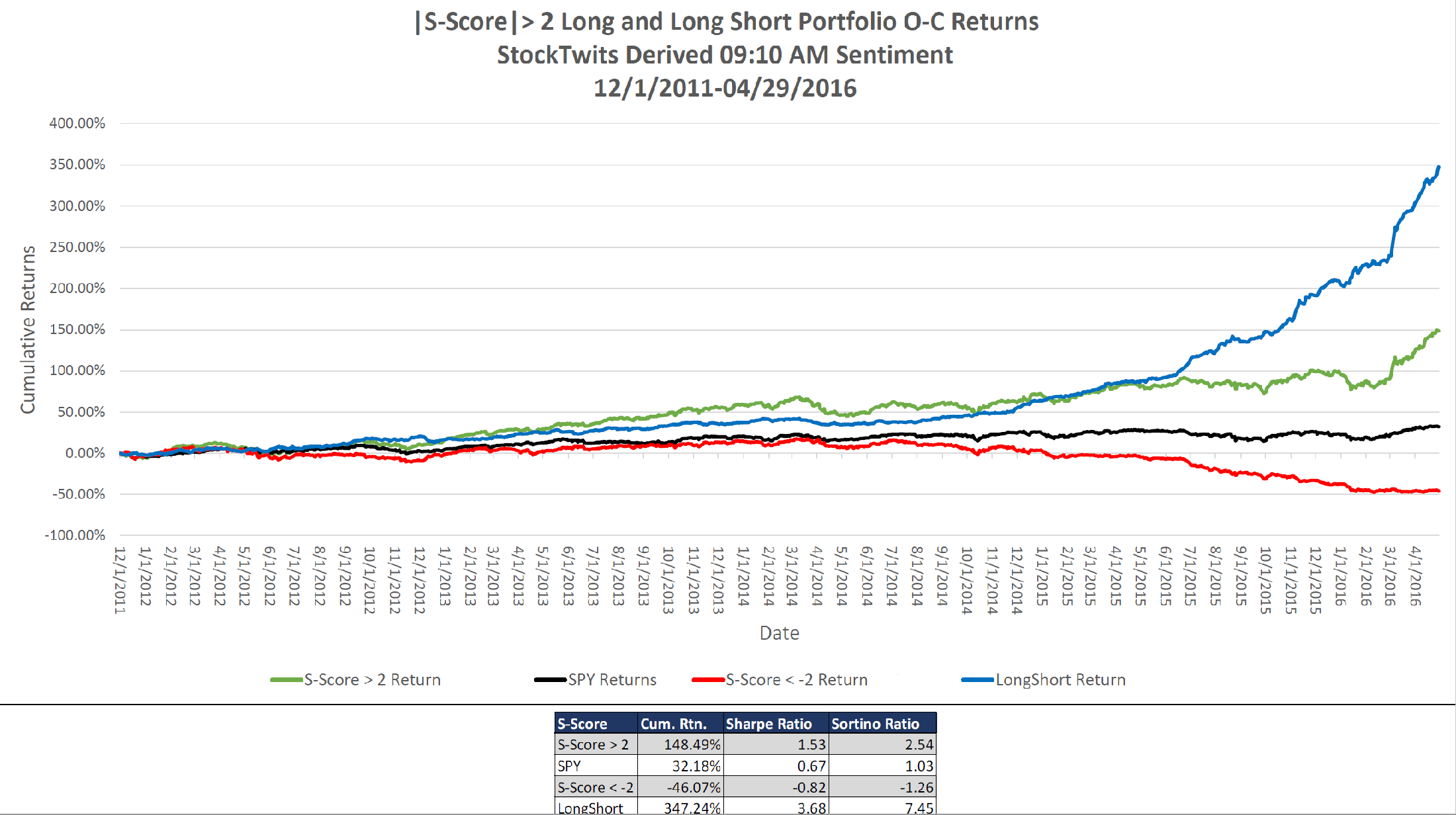

Social Market Analytics (SMA) aggregates the intentions of investors as expressed on the StockTwits platform. SMA creates proprietary S-Factor metrics that quantitatively describe the current conversation relative to historical benchmarks. This data provides strong predictors of future price movement. This blog will focus on the deterministic nature of the StockTwits data set when aggregated into SMA S-Factors. StockTwits is a community for active traders to share ideas enabling you to tap into the pulse of the market: http://stocktwits.com/

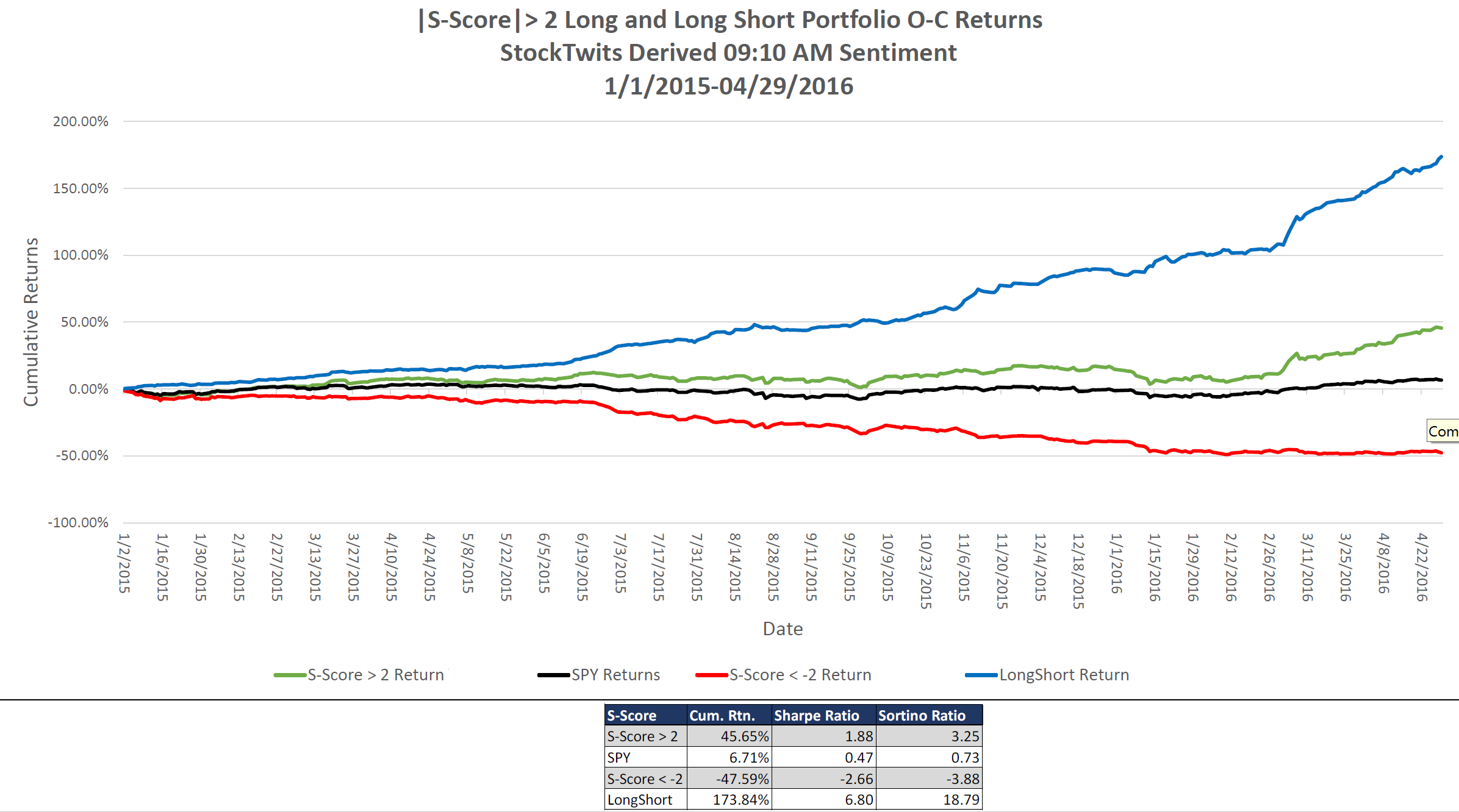

The charts and tables below illustrate the subsequent open to close return of stocks that are being spoken about abnormally positively or abnormally negatively on StockTwits twenty minutes prior to market open. Sharpe and Sortino ratios for the theoretical portfolios are included as well. The SMA S-Score looks at the current conversation relative to historical benchmarks and creates effectively a Z-Score.

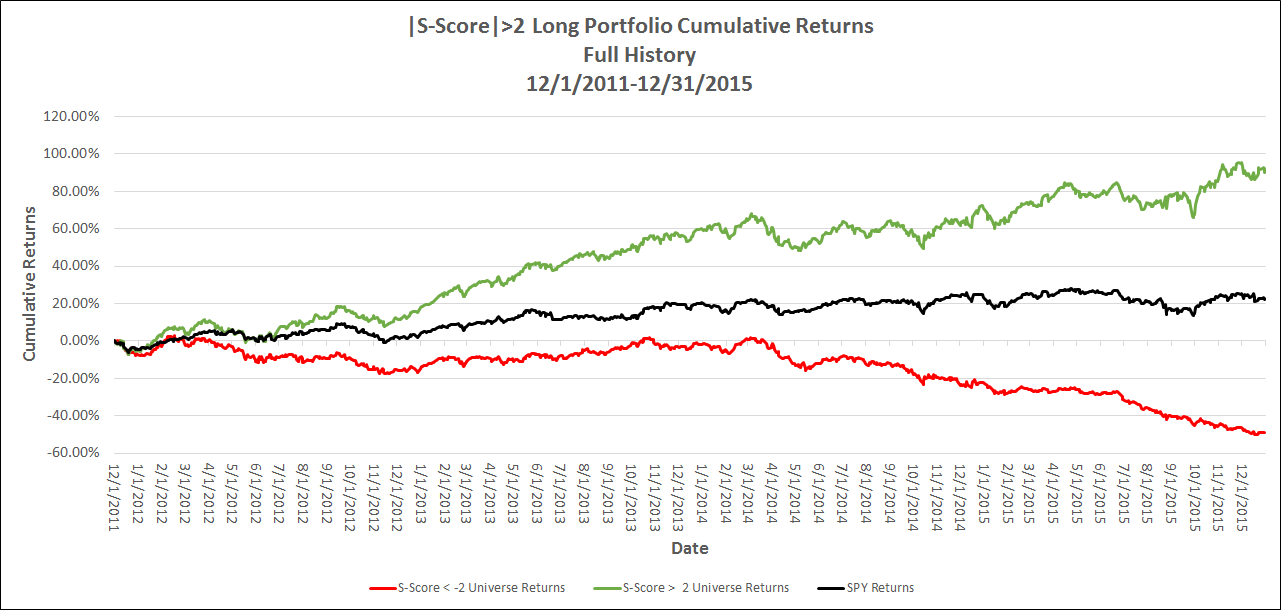

The Green line below is an index of subsequent open to close return of stocks with abnormally positive conversations on StockTwits prior to the market open. The Red line is an index of the subsequent open to close return of stocks with an abnormally negative conversation prior to market open. The black line represents the market open to close return and the blue line represents a theoretical long/short portfolio.

These charts clearly illustrate the predictive information present in the StockTwits message stream. If there was no predictive power in the StockTwits data set the Green, Red, and Black lines would be nearly identical -statistically not the case. These signals are available at 9:10 am Eastern time well before the market open.

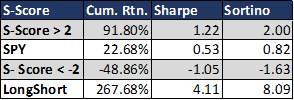

The chart below looks at the full SMA history of StockTwits based S-Factors. The theoretical long portfolio has a Sharpe Ratio of 1.53, theoretical short portfolio -.82 Sharpe and LS portfolio has a Sharpe of 3.68. Sortino Ratios are above one as well. There is strong predictive power in this data.

The last year has been particularly challenging for the Hedge Fund community. Below is a chart with the performance of the theoretical portfolios broken out from 1/1/2015 to current. As you can see these portfolios performed well in this volatile market period.

For more information on these data sets please contact Pierce Crosby: (pierce@stocktwits.com) or Joe Gits: (joeg@socialmarketanalytics.com)

Regards,

Joe

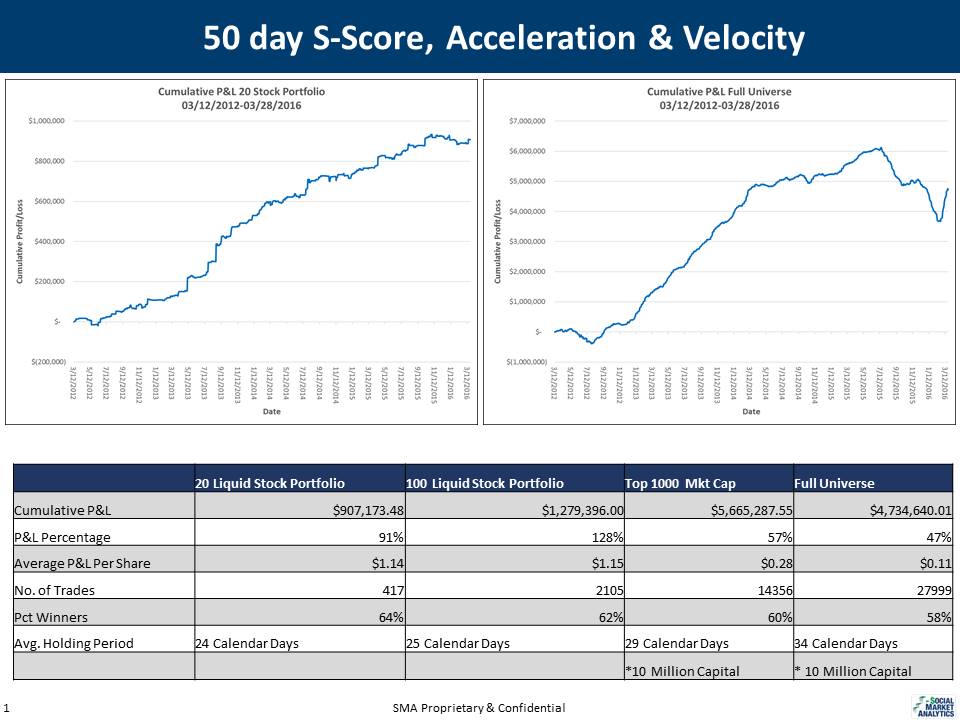

Signals derived from Twitter data have typically been viewed as shorter term signals. There are a number of reasons for this. One reason is the lack of out of sample data to back test trading systems on. At SMA we now have nearly four and a half years of sentiment metrics to use in the creation of longer term signals. Long-Term is a subjective term when discussing holding periods. For our purposes we will be looking at trading signals that generate an average holding period of one month to three months.

At SMA we do not believe that one metric provides the full tone and context of a Twitter conversation. That is why we publish a family of metrics call S-Factors that provide a richer view of the conversation than what is available with a single metric.

With history we have been able to look at longer term metrics and changes in security prices over longer periods. We looked at large rapid negative changes in sentiment and determined that these sentiment movements are overreactions and lead to buying opportunities. We introduce two new metrics: Velocity and Acceleration. The universes for these back test range from 20 large Twitter followed liquid stocks to the entire equity universe. As you can see below these strategies identify solid buying opportunities and generate healthy average profit per share. Please contact SMA to learn more about using sentiment to generate longer holding period trading signals with sentiment data.

Below are equity curves and trading statistics net of commissions with various universes. Overall you generate much fewer trades and hold them for longer periods of time. The 50-day S-Score chart uses the SMA S-Score, Velocity and Acceleration Metrics. You see that the holding periods are much longer than signals typically generated by social media. The columns represent different universe sizes.

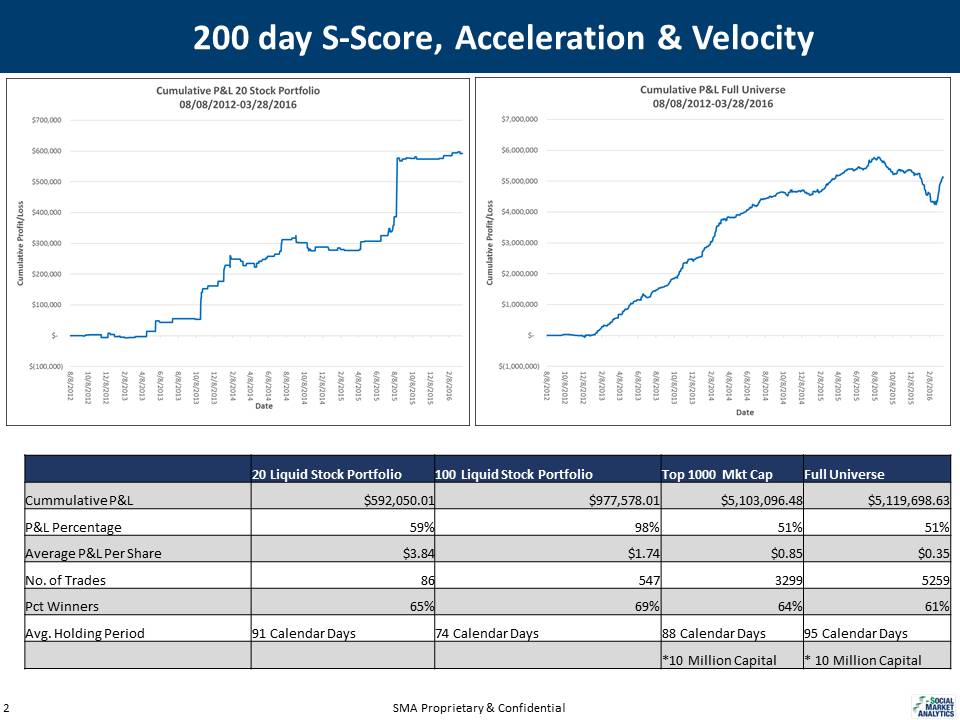

200 Day S-Scores returns are below. Again, please contact SMA for more detailed information.

To learn more please contact us at: ContactUs@SocialMarketAnalytics.com

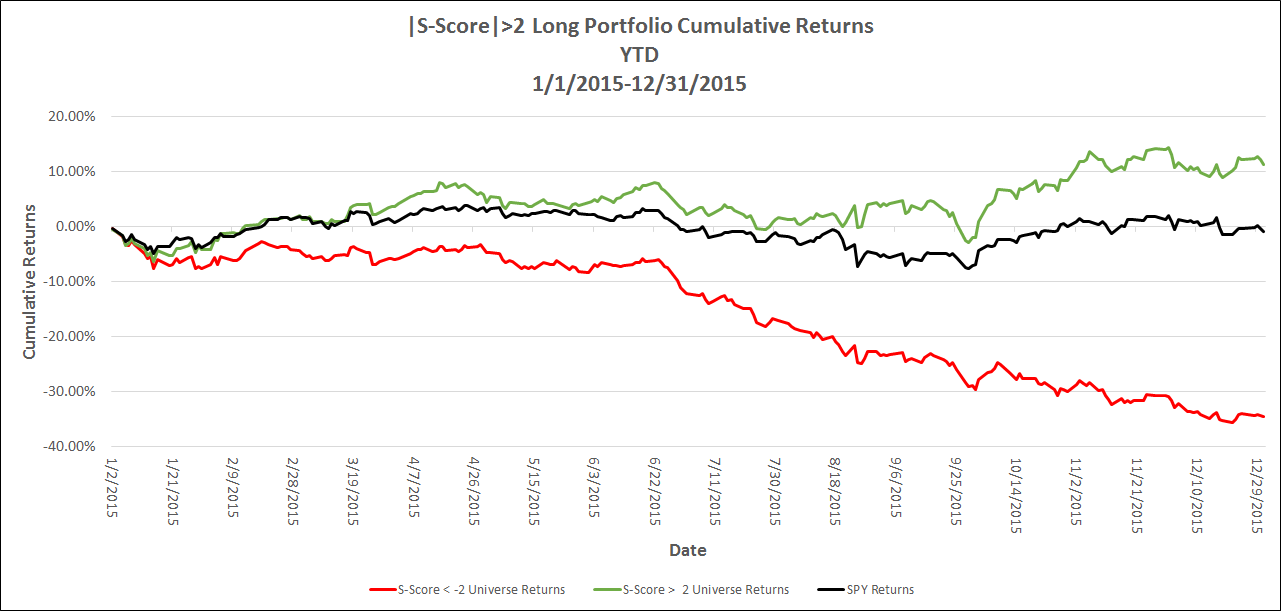

Wow, what a ride 2015 was with the S&P 500 closing slightly down for the year. As we head into 2016 are you going to continue to look at the same factors as everyone else or maybe try something new?

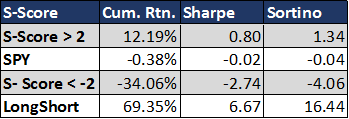

Below are the returns for stocks with significantly positive and negative pre-market open S-Scores. Stocks with High pre-market open sentiment scores had a cumulative return of 12.19% versus an SP 500 open to close return of -.38%. Stocks with a low pre-market open sentiment score had a cumulative open to close performance of -34%. Stocks with high sentiment scores outperformed and stocks with low sentiment scores under-performed. With significant Sharpes and Sortinos. Combining S-Factors with your selection criteria and risk management can add a dynamic new factor to your security selection.

These charts use the S-Factor S-Score. SMA publishes and family of S-Factors to clearly identify the tone of the social media conversation. To learn more go to: https://socialmarketanalytics.com/process.

Social Market Analytics has been publishing the performance characteristics of stocks with high and low sentiment over the last four years. Last year it was difficult to find success with traditional factors. SMA S-Factors helped our customers generate out-performance. Please contact Social Market Analytics to explore how sentiment based factors can be included in your models: ContactUs@SocialMarketAnalytics.com.

People ask about the persistence of SMA sentiment signals over time. The signal length is dependent on the S-Factor used. S-Mean for example represents a 20 day look back period and is generally used as a longer term signal. We looked at a theoretical strategy using a universe of the Russell 1000 and S-Factors: S-Score, S-Volume and price. It is not intended as a proposal of a trading strategy using S-Factors as a single factor in an alpha model it does illustrate the persistence of the signal over time.

We primarily looked at the signal prior to market open instead of prior days close to include the most recent social media conversation in the metrics. If you use a sentiment score from the prior days close you don’t include overnight information such as news, foreign markets, and indication of market open…

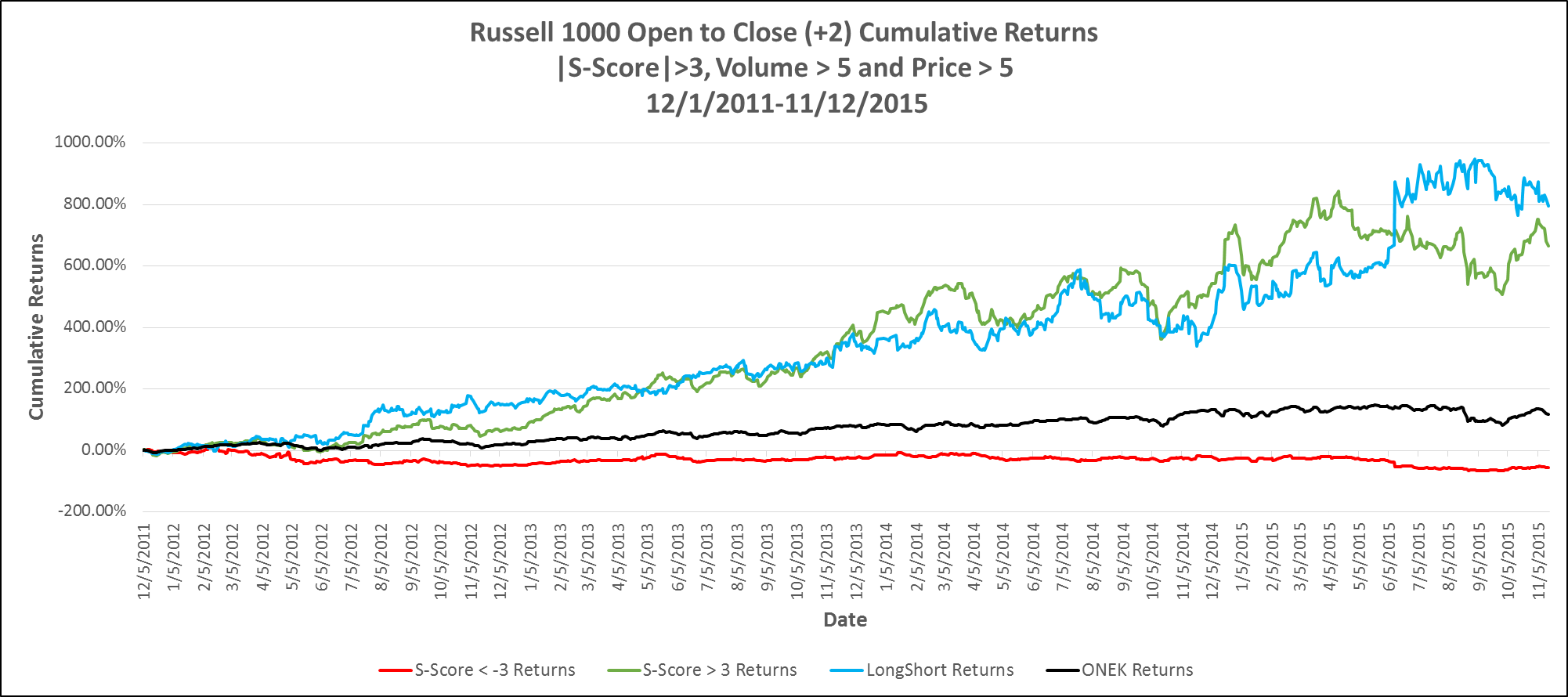

The universe of stocks considered is the Russell 1000 representation as of 06/26/2015. The back test period is 2011-12-01 to 2015-11-12. There are no transaction costs/impact costs assumptions included in this analysis.

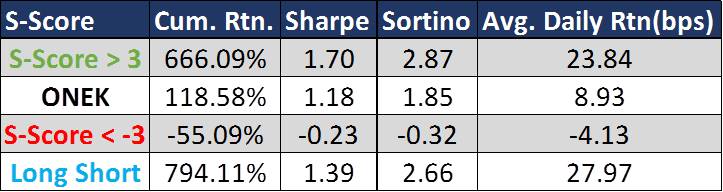

The simulation uses S-Score > 3 / S-Score < -3 AND S-Volume > 5 AND Price at Entry > $5. An S-Score > 3 means the current conversation is more positive than 99% of conversations over the look back period (20 days). The reason for choosing the threshold of 3 for S-Score is motivated, in part; on research results presented by Markit using the SMA S-Factors (contact us for the research). The position holding period is Open to Close (+2), (i.e. close 2 business days from now). The S-Factors signals used were selected at 09:10 AM (ET).

In the below chart, the Green Curve shows the results of going long on Positive Signal (S-Score positive with the thresholds used). Similarly, the Red Curve shows the returns of the negative (S-Score <-3, negative return is good in this case). The Blue Curve is the result of going long on Positive Signal Portfolio and short the Negative Signal Portfolio each day. Black Curve is the ONEK ETF (Russell 1000 SPDR ETF) and serves as a market reference for the back test period. Risk adjusted performance measures (Sharpe, Sortino) and average daily returns are presented for each filter.

The results of Open to Close (+2) Strategy using |S-Score|> 3 & S-Volume > 5 & Entry Price > $5 signal at 09:10 AM are below. To test the strength of a signal with strong threshold, we decided to hold the position for 3 days, (buying at the open when the signal met requirements of the filter and selling it at the close 2 business days later). If a stock appears on 2 consecutive days, the trades are made in isolation, irrespective of the position that is held due to previous signal. The Positive and Long Short outperform the ONEK benchmark. A large spread between Positive results and the benchmark is evident.

In our simulation the positive S-Score portfolio returns 23 bps per day versus the benchmark of 9 bps per day. The long/short portfolio returns 28 bps versus the 9 bps per day for the benchmark. Certainly significant reason for further analysis of adding sentiment signals to your portfolio.

These results illustrate that adding S-Volume and price filters, in conjunction with S-Score, yields significant positive returns performance.

Please contact us for much more detail and other back test or to explore how sentiment metrics can be used in your environment.

Social Market Analytics has been offering API access to our data since inception. Fewer people know we also offer powerful visualization and screening tools. We offer two ways to access our data without programming.

First, we have a robust Excel Add-in that allows for Real-Time screening and historical retrieval. This functionality is ideal for integrating sentiment data into Excel based research platforms. You can screen for user defined pricing and sentiment criteria or upload a watch list and monitor sentiment activity on these securities in real-time.

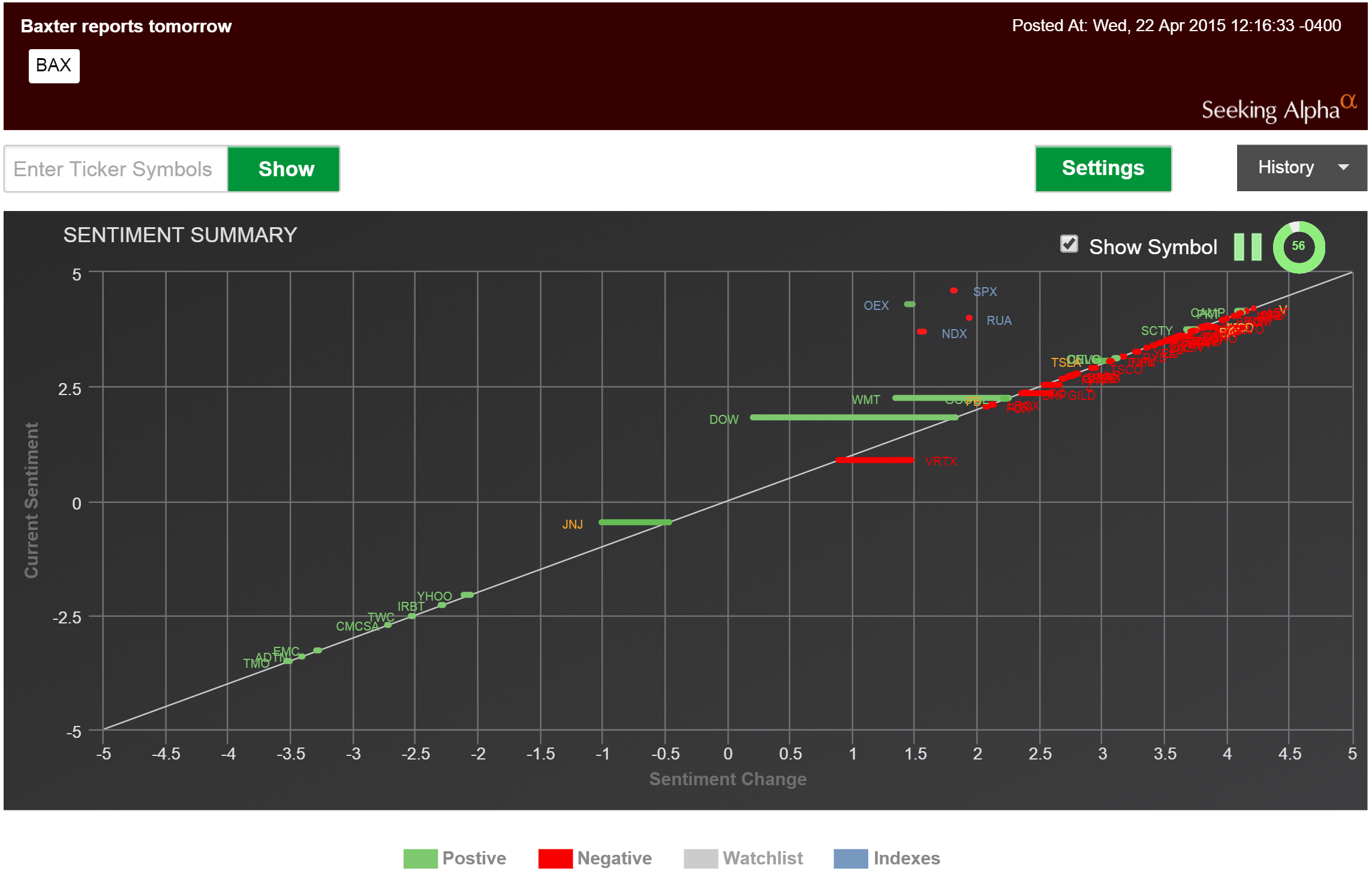

The SMA Sentiment Dashboard is a real-time visual representation of sentiment changes for the entire universe or your watch list. the below screen provides a real-time view of stocks with large changes is social media. Users can set criteria for filtering for the most relevant securities.

The dashboard tracks sentiment for Stocks, commodities, currencies, indexes, sectors and industries. Below is an illustration of industry level sentiment.

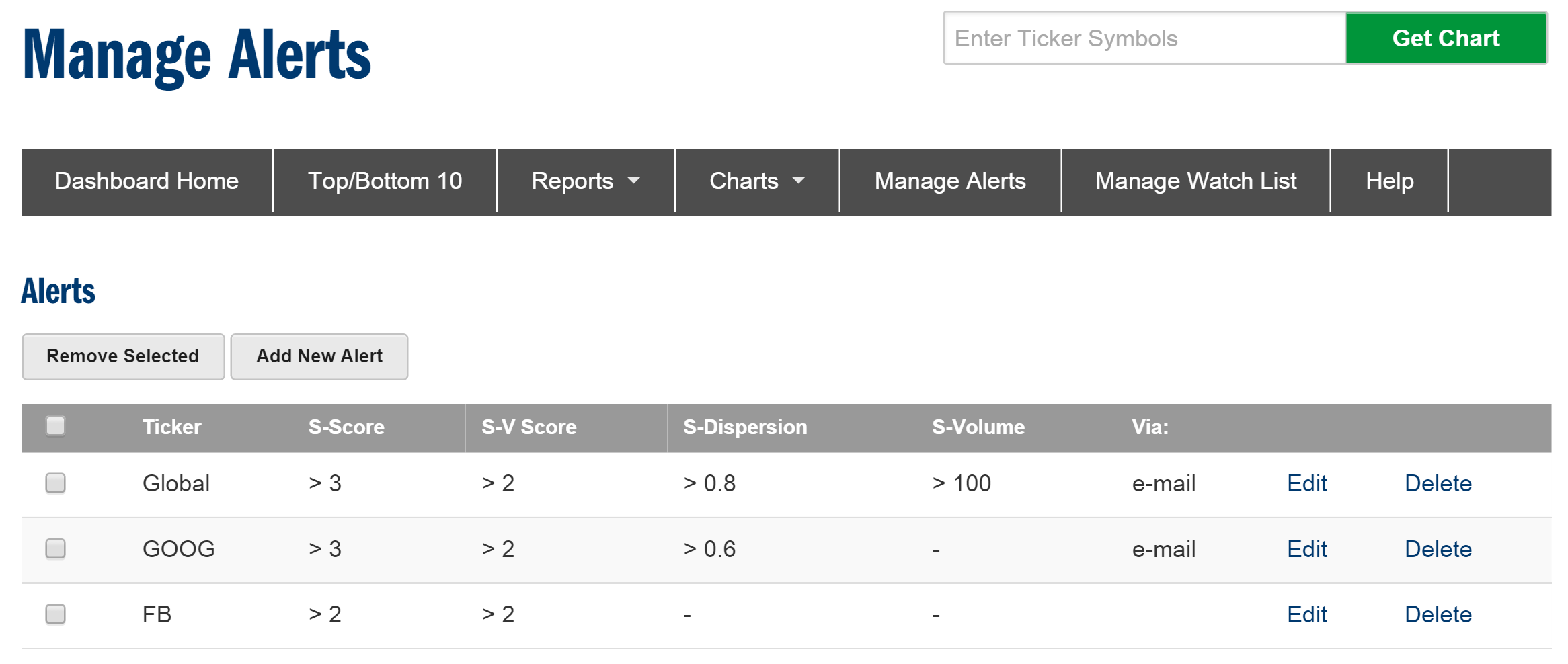

In, addition users can set screening criteria for real-time alerting by email, text or private Tweet. Alerts can be specified for individual securities, watch list of securities or the entire universe.

These are just some of the visualization tools SMA offers. For a full demonstration of trial contact us at Sales@SocialMarketAnalytics.com

Thanks,

SMA

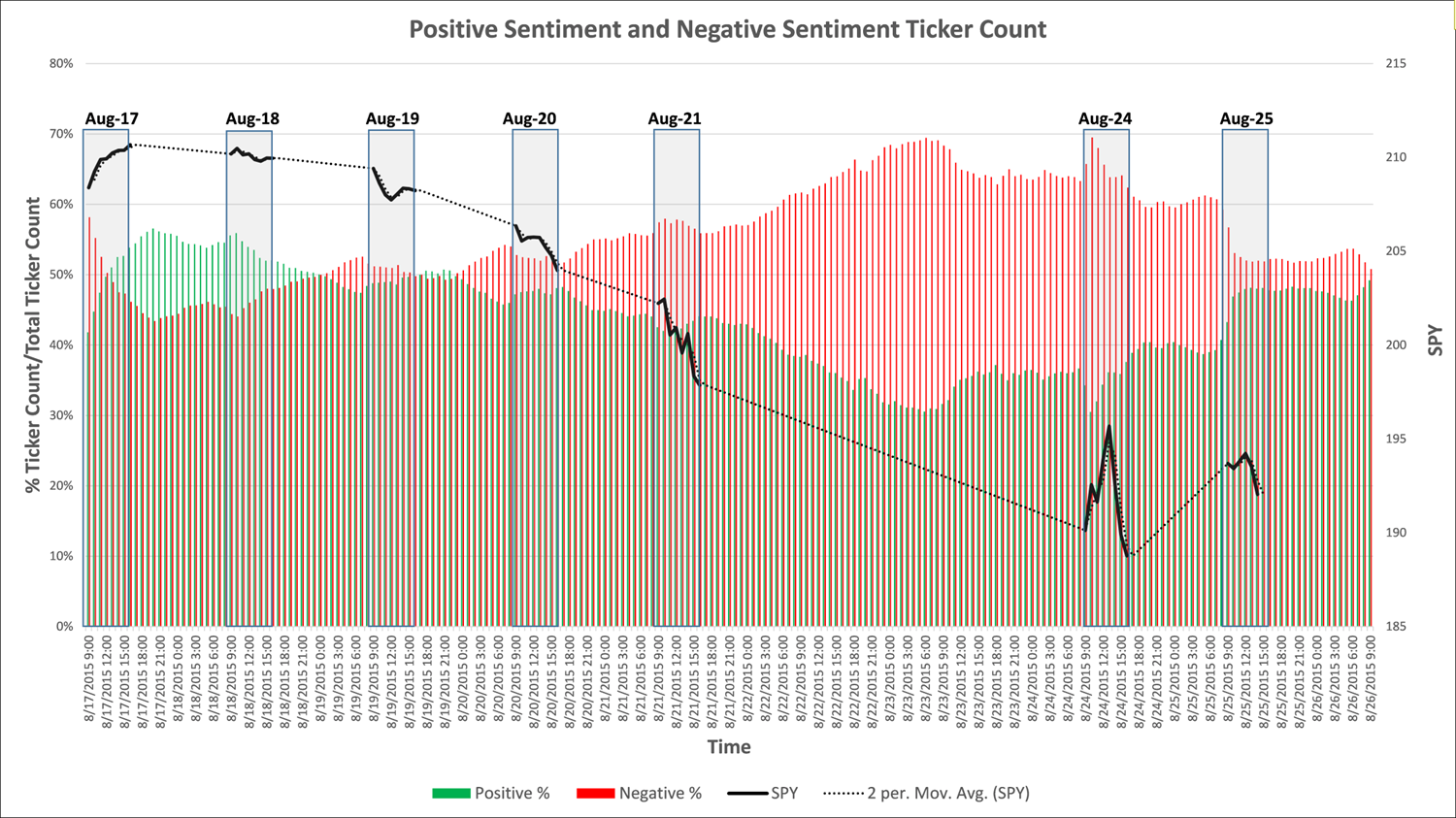

The chart below looks at the percentage of positive Tweets versus the percentage of negative Tweets over the last couple of weeks. There are usually significantly more positive than negative Tweets so the fact that the negative percentage was so high is valuable data in itself. As you can see the percentage of negative Tweets increased prior to days with significant market downtrends.

The black lines on the chart represent market activity. The red and green bars represent negative and positive Tweet percentages. Sentiment is captured by Social Market Analytics 24×7; you can see the growth in negative sentiment prior to the Monday (8/24 draw down). On 8/24 the market started strong and fell significantly at session end.

The universe of Tweets is so large that when you aggregate it you get a terrific view of what people believe is going to happen. This data is only available from Social Market Analytics. Please contact us for more information on our market leading data sets or visit our Research Page.

Thanks,

Joe

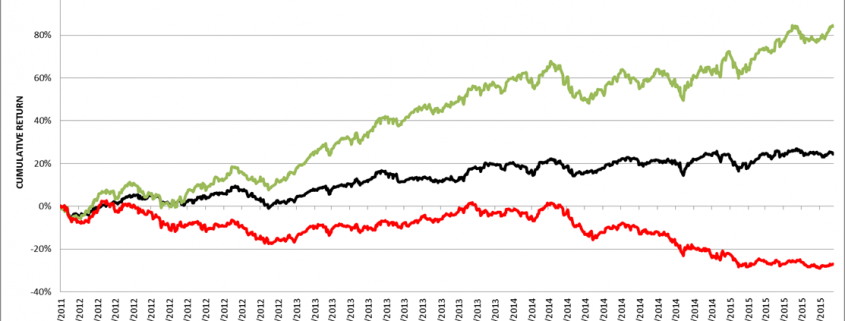

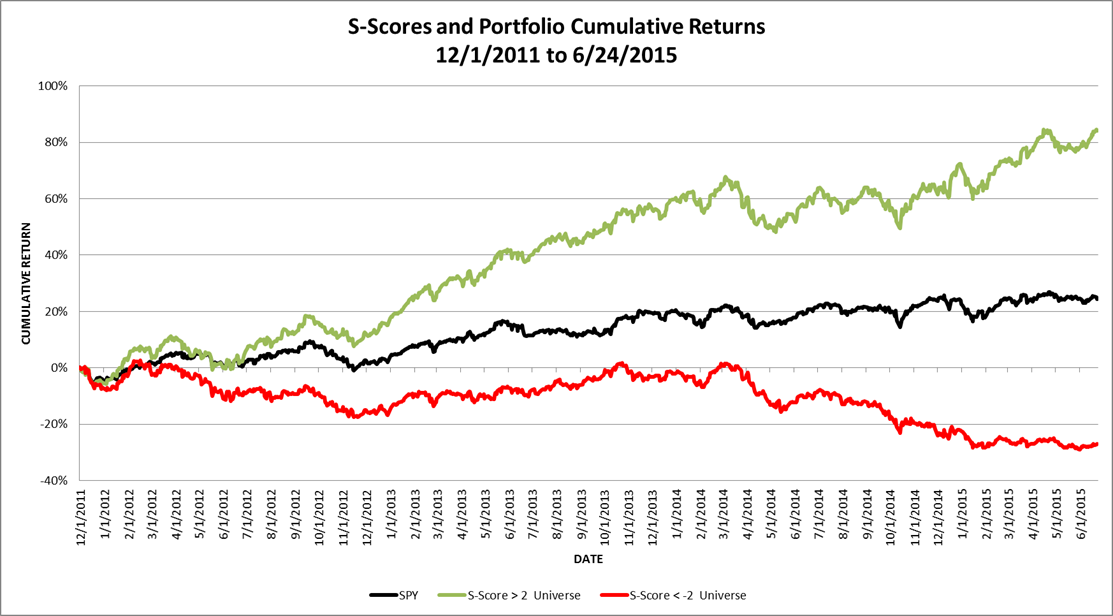

Every quarter we review performance returns and statistical ratios for our family of S-Factors. S-Score is a normalized representation of sentiment over a pre-defined look back period and is a key metric. Below are some charts that look at the full history and YTD performance of our data across the entire universe.

Anyone can pick specific securities and instances where sentiment leads price movement; it’s a lot harder to consistently predict movements over the entire universe over a long period of time. We pride ourselves on statistical consistency of our data over what is now 3.5 years of history. We are the only company to track and publish these metrics, providing the most transparency.

We view S-Score >2 and S-Score <-2 as statistically significant. An S-score of 2 means the current conversation on social media is more positive than 97 percent of prior conversations as filtered by our proprietary metrics. When this happens the security moves higher with statistically significant consistency. The green line below represents the full history cumulative open to close return chart of stocks with a high S-Score (S-Score >2) prior to market open. The Red line represents the full history cumulative open to close return of stocks with an extreme negative S-Score (S-Score <-2) prior to market open. The black line represents the open to close return of stocks in the SP500. The Sharpe and Sortino ratios for the green line (Pre-Open S-Score >2) are 1.37 and 2.23 respectively. Sharpe and Sortino ratios for the red line (Pre-Open S-Score <-2) are -.54 and -.86. Benchmark SP500 Sharpe = .69 and Sortino = 1.08.

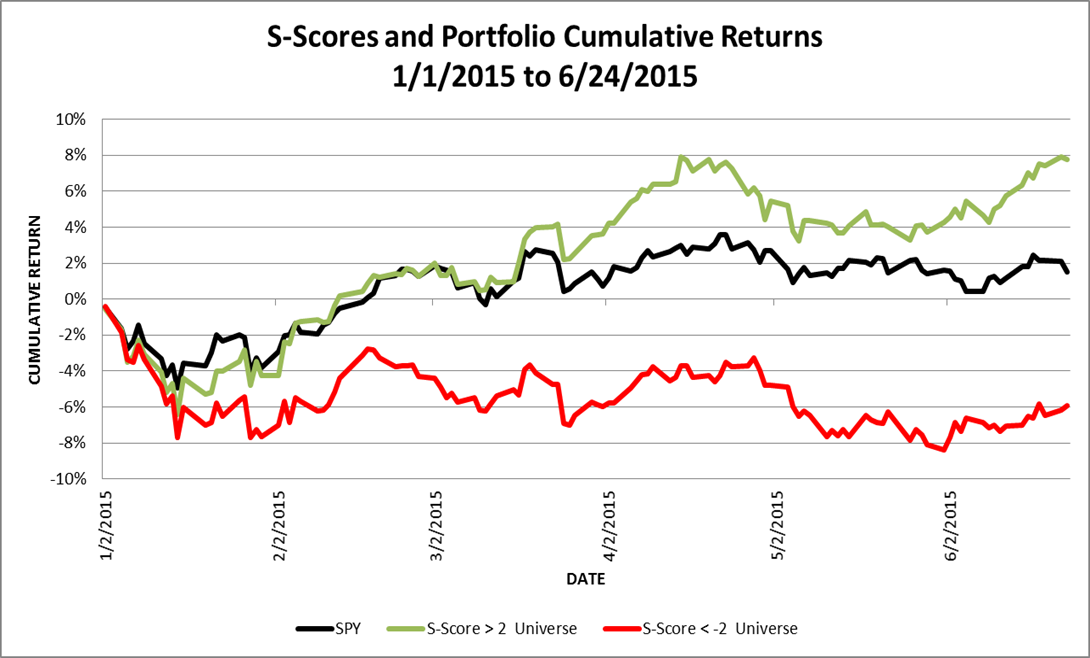

Below is the exact same chart for YTD 2015. Sharpe and Sortino ratios show the benefit of our evolving filtering and scoring criteria.

Price and Tweet volume filters are commonly added when filtering stocks for sentiment. Tweet volume represents indicative Tweet volume, once all Tweets are filtered indicative volume typically represents only 10% of the total volume of Tweets. The below chart is the same return chart represented above with the added filter of Price day close price >5 and indicative Tweet volume > 5. As you can see the Sharpe and Sortino ratios increase dramatically by adding simple filters.

Social media analytics is a learning process. Our filtering and cleansing algorithms are continuously evolving. We maintain our history as it was at each time and we keep dictionaries and accounts as a time series.

We have many more statistics employing other S-Factors and filtering criteria; please contact us for a more detailed briefing on SMA data and products.

Thanks,

Joe