Signals derived from Twitter data have typically been viewed as shorter term signals. There are a number of reasons for this. One reason is the lack of out of sample data to back test trading systems on. At SMA we now have nearly four and a half years of sentiment metrics to use in the creation of longer term signals. Long-Term is a subjective term when discussing holding periods. For our purposes we will be looking at trading signals that generate an average holding period of one month to three months.

At SMA we do not believe that one metric provides the full tone and context of a Twitter conversation. That is why we publish a family of metrics call S-Factors that provide a richer view of the conversation than what is available with a single metric.

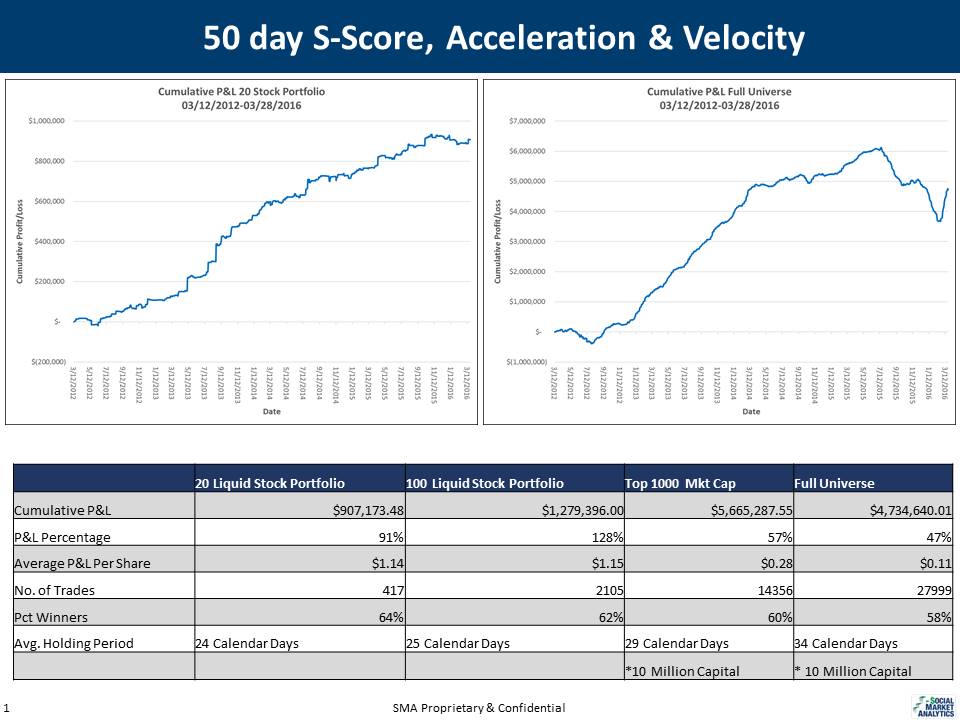

With history we have been able to look at longer term metrics and changes in security prices over longer periods. We looked at large rapid negative changes in sentiment and determined that these sentiment movements are overreactions and lead to buying opportunities. We introduce two new metrics: Velocity and Acceleration. The universes for these back test range from 20 large Twitter followed liquid stocks to the entire equity universe. As you can see below these strategies identify solid buying opportunities and generate healthy average profit per share. Please contact SMA to learn more about using sentiment to generate longer holding period trading signals with sentiment data.

Below are equity curves and trading statistics net of commissions with various universes. Overall you generate much fewer trades and hold them for longer periods of time. The 50-day S-Score chart uses the SMA S-Score, Velocity and Acceleration Metrics. You see that the holding periods are much longer than signals typically generated by social media. The columns represent different universe sizes.

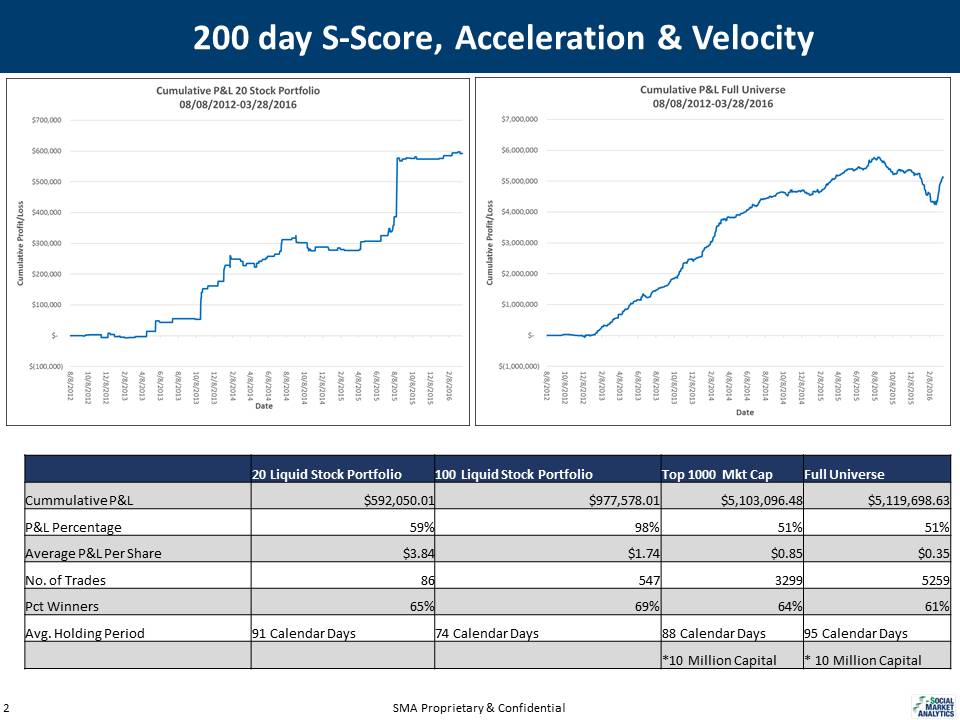

200 Day S-Scores returns are below. Again, please contact SMA for more detailed information.

To learn more please contact us at: ContactUs@SocialMarketAnalytics.com