Machine Readable Filings (MRF) Extract the Significance of ESG in Future Earnings

August 4, 2020

Discussions of Environmental, Social and Governance (ESG) has grown exponentially in the last few years. Socially conscious investors believe ESG criteria better determine the future financial performance of companies. There is a growing number of ESG funds, ETFs and other products based on ESG. To determine whether the increase in ESG discussions have influenced company operations, SMA analyzed the breadth ESG mentions in SEC Filings using ‘Machine Readable Filings’ (MRF).

Social Market Analytics, Inc. (SMA) has partnered with S&P Global Market Intelligence on ‘Machine Readable Filings’ (MRF). MRF is the first product to provide parsed textual data of SEC Edgar Regulatory Filings at the Item, Section, Sub-section, and Notes level with historical baselines back to 2006. Extraneous information such as page numbers, images, and tables are removed. SMA is currently developing the same structured data on International Reports which will be released in Q4 2020.

SEC filings are formal documents reported to the U.S. Securities and Exchange Commission (SEC) that contain important information about Companies, such as Management Discussion & Analysis and Risk Factors. Every U.S. publicly traded company is required to submit regulatory filings.

SMA’s proprietary Topic Modeling allows us to analyze mentions of ESG within MRF, while filtering out the unfitting noise. The ESG Topic Models captures every mention of “ESG” within SEC filings, including related terms using statistical synonym capabilities while filtering out mentions of “ESG” where it does not apply to Environmental, Social and Governance. For example, mentions of an internal group called Energy Services Group abbreviated as “ESG” in Halliburton Company’s regulatory filings would not be included in the ESG Topic Model. The ESG Topic Model flags the filings matching the topic model criteria since 2006 and extracts the textual context of the mention of the ‘ESG”-related phrase to analyze who is talking about ESG and how they are talking about it.

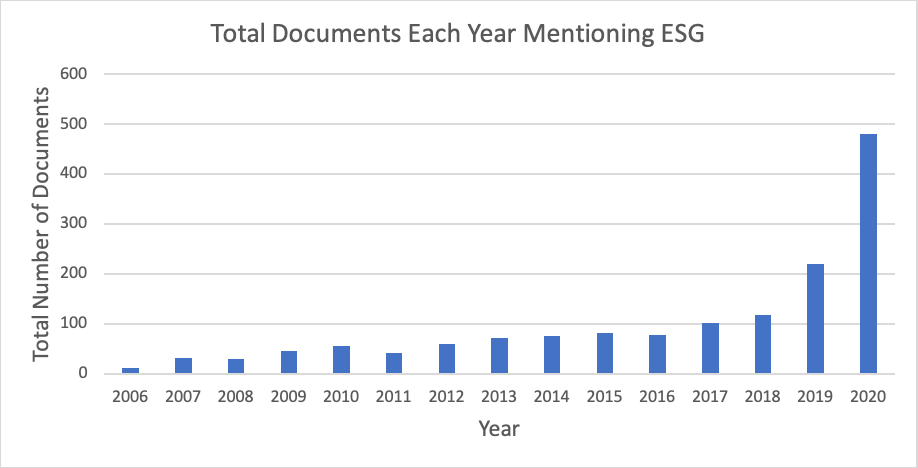

The first step in analyzing the dataset was to see the trend since 2006. In order to see the growth in conversation of ESG, we charted the total number of unique documents each year, based on the year the document is published. The chart demonstrates exponential growth since 2006. The least number of documents published in a year that mention ESG was in 2006 with 12 documents and the most is in 2020 with 481 documents as of July 23. The total amount of documents mentioning ESG since 2006 is 1,502.

When companies mention ESG in their filings, the mentions tend to be in 10-Ks where companies typically go into the most detail. Of the 1,502 documents that mention ESG, 683 documents were 10-Ks or 10-K/A and 291 were 10-Qs or 10-Q/As. There are about 3x as many 10-Qs total than 10-Ks because of how often they are reported each year. 2020 is by far the largest year, and more companies will mention ESG in 10-Q filings reported over the next two quarters. Occasionally 8-K filings will mention ESG when there is a new ESG initiative or update.

In order to validate that few companies are not releasing many filings mentioning ESG, we calculated the number of unique companies mention ESG each year. The number of unique companies each year shows parallel exponential growth to total documents. ESG initiatives are spreading across many companies. There are a total of 597 different companies reporting filings that mention ESG since 2006. This validates that the documents with mentions of ESG are not dominated by few companies. It also makes sense there is not bias towards one company because most of the documents mentioning ESG come from 10-K filings which companies only release once a year.

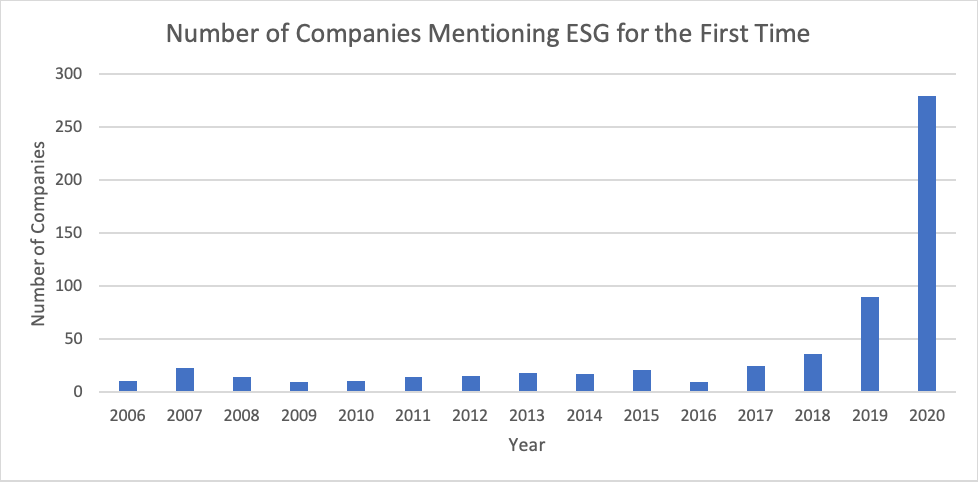

We then wanted to look at when companies mention ESG for the first time. Almost half (279/597) of the companies in our dataset were flagged by the topic model for the first time in 2020. Between 2006 and 2018, new companies mentioning ESG for the first time in their filings was between 10 and 36. In 2019, the amount of new companies mentioning ESG in their filings jumped to 290, almost tripling the highest year before. In 2020, that number more than tripled again. Still only 579 companies have mentioned ESG to date which is about 15% of publicly traded U.S. companies.

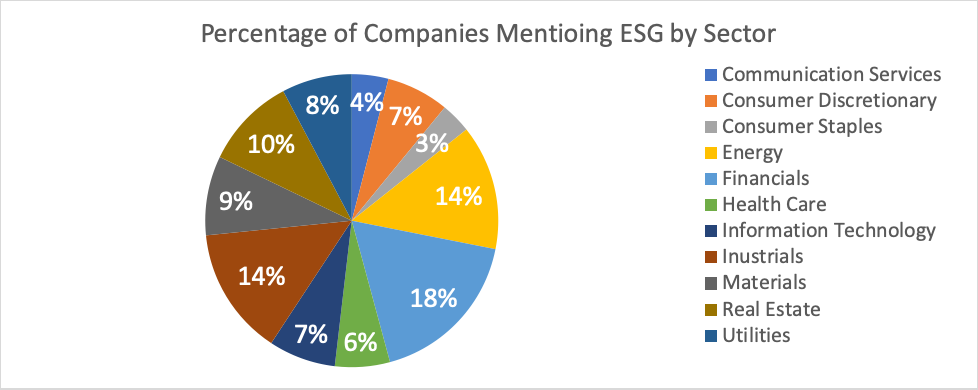

Since few companies are mentioning ESG in their filings, we then looked at the data by sector to see if there is a trend. The three largest sectors mentioning ESG are Financials, Energy and Industrials. The Financials industry primarily talks about products offered or investments in companies that are thought to value ESG more. Energy and Industrials could be companies that are required to practice environmentally friendly procedures within their business model. The two smallest sectors are Communication Services and Consumer Staples. The two sectors are not as impacted by economic cycles, therefore could be more resistant to economic trends.

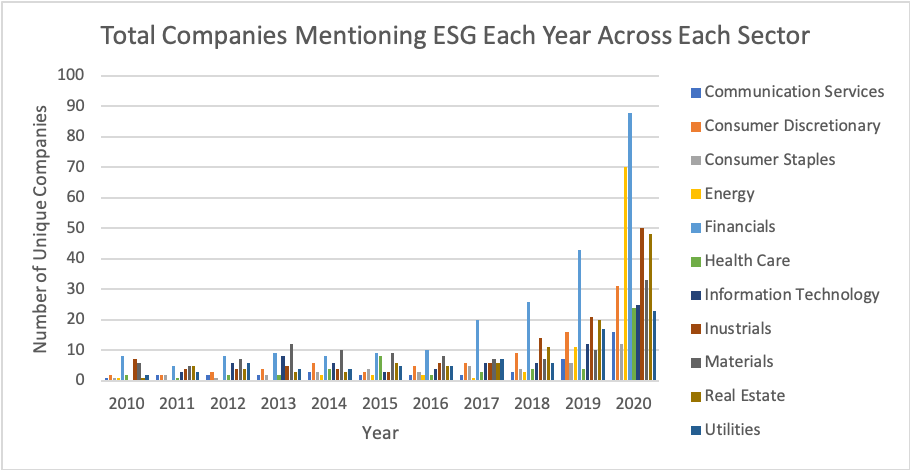

After looking at the share of companies mentioning ESG by sector, we decided to see if there was a trend over time. The Financials sector has been the clear leader in having the most companies mention ESG in filings for the last 5 years. However, the second leading sector, Energy, had not been nearly as high until 2020. Before 2020, the Energy sector had an average of less than 2 companies per year mentioning ESG in their filings and had only the 7th most companies mentioning ESG in 2019, which indicates there may have been an increase in public or investor pressure to mention ESG in their filings. Prior to the surge in the Energy sector mentioning, the Industrials and Real Estate sectors had been going back and forth for the last couple years for the second and third most companies that mention ESG in their filings. The growth rate was much less spontaneous than the Energy sector.

ESG is a growing topic for both Companies and Investors and has been increasing exponentially within SEC filings. The number of companies mentioning ESG in their filings has been growing dramatically over the past four years. We expect this trend to continue as investors become more socially conscious in their investing. Companies tend to discuss ESG in their most detailed documents, either 10-Ks or 10-Qs. The sectors mentioning ESG the most are Financials, Energy, Industrials and Real Estate. The greatest recent surge in companies has come from the Energy sector. Utilizing MRF and the Topic Models built to analyze the dataset, Firms can get a better picture of which companies are truly ESG conscious.

As the breadth of companies widens and the depth of ESG mentions increase in Filings, we believe ESG will drive investor returns. We believe MRF will become an important tool for Asset Managers to evaluate ESG as part of their investment strategy. In future blogs we will explore the relative return of companies with and without ESG principles.

For more information about Social Market Analytics ContactUs@SocialMarketAnalytics.com. By David Stolz