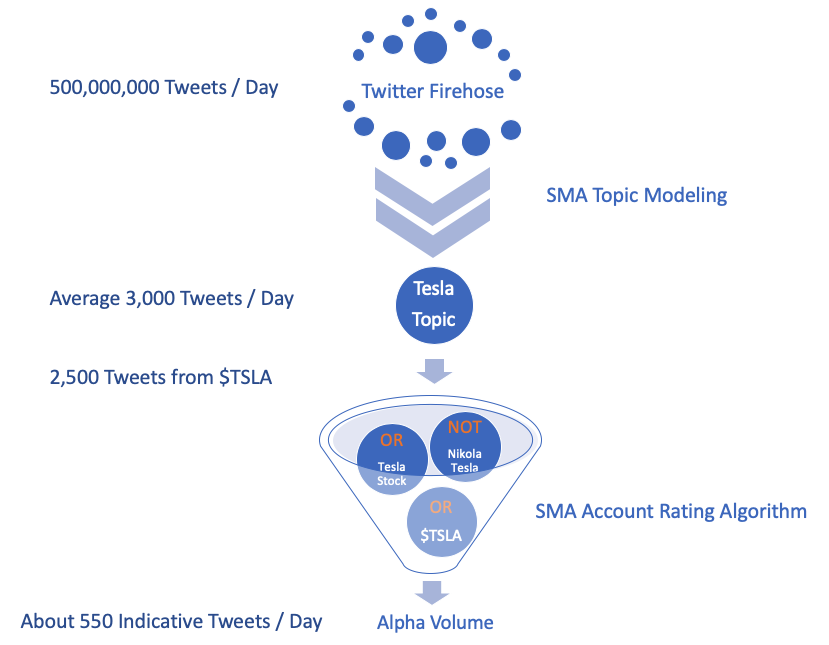

At Social Market Analytics we use proprietary techniques to return the most accurate Twitter volume for topics of interest. First, we use a topic model not just $Ticker. Most vendors use the CashTag concept to identify securities. At SMA we believe only using CashTag excludes a lot of valuable conversation. We return higher volume and cleaner conversations because we use a machine learning rules based system to return all conversations about a security that are not tagged with $Ticker. In the diagram below we return about 500 extra Tweets a day for Tesla Motors versus just $TSLA. Our topic model evolves with the conversation over time.

After applying our topic model filter we additionally filter Tweets based on our proprietary account validation metrics. Only Tweets from our SMA approved accounts are included. In the below example, there are about 500 Tweets for Tesla Motors from the certified accounts per day. These accounts pass our multi-step algorithm. One metric we use is weighted accuracy over time. For example, when a Twitter account is bullish on a security what percentage of time does that security subsequently move higher.

Below is a visualization of SMA Twitter filtering process for the Tesla topic.

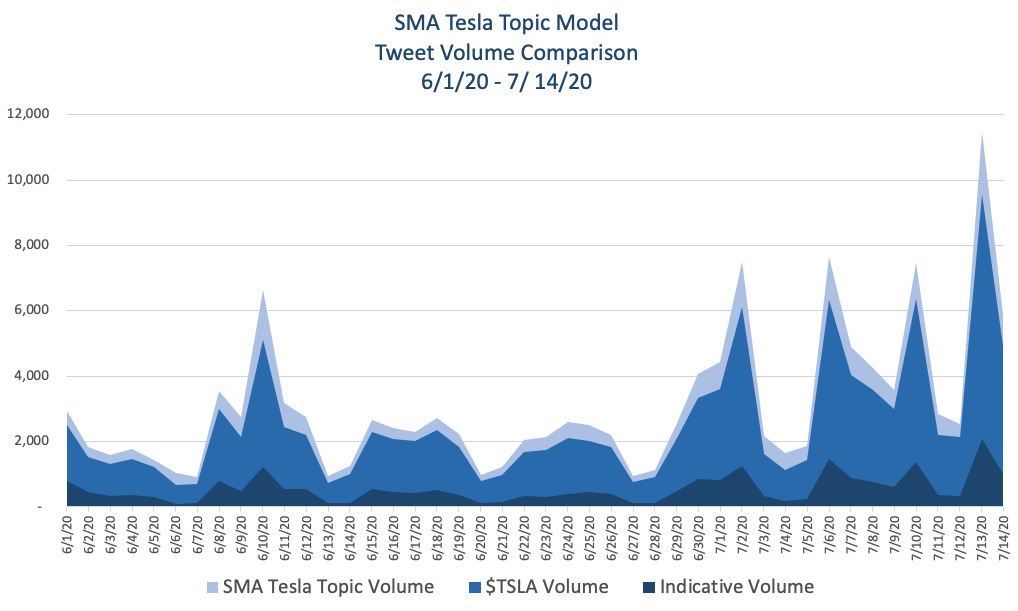

Below is a time series of Tesla Topic model versus $TSLA with the additional filter for SMA certified accounts.

As you can see from the charts SMA’s proprietary technology provides the truest view of the each securities topic model. To learn more about our technology or receive a sample data set ContactUs@socialmarketanalytics.com.

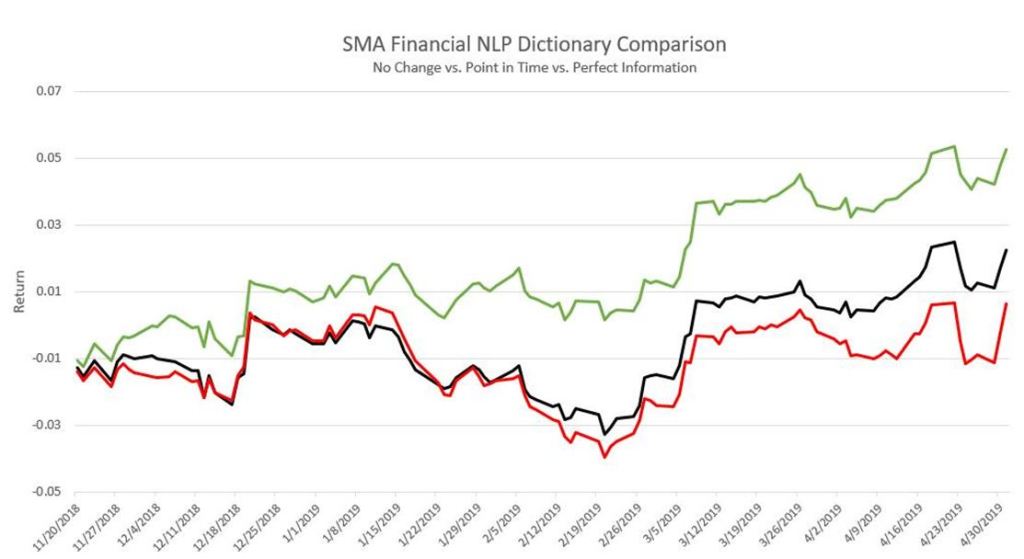

Please contact us with any questions or to see how SMA’s NLP and filtering capabilities can be used in your investment process. ContactUs@SocialMarketAnalytics.com

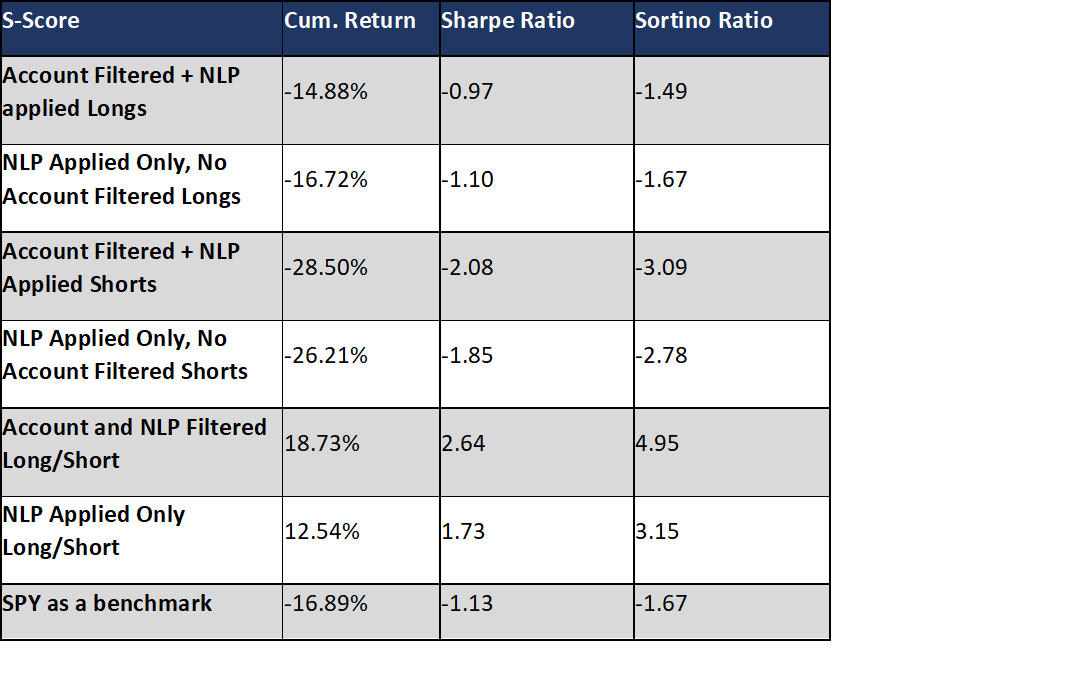

Please contact us with any questions or to see how SMA’s NLP and filtering capabilities can be used in your investment process. ContactUs@SocialMarketAnalytics.com