A Leader in Unstructured Financial Data

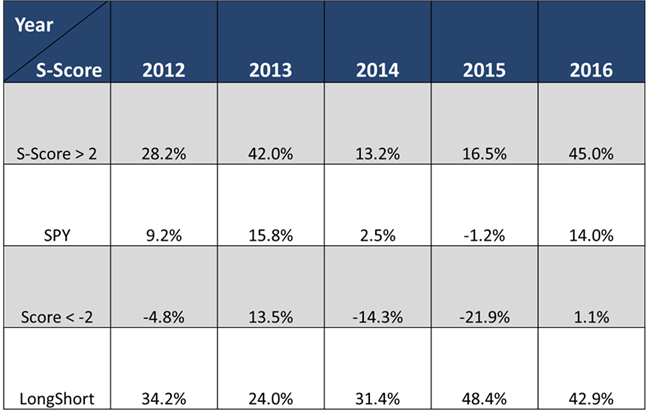

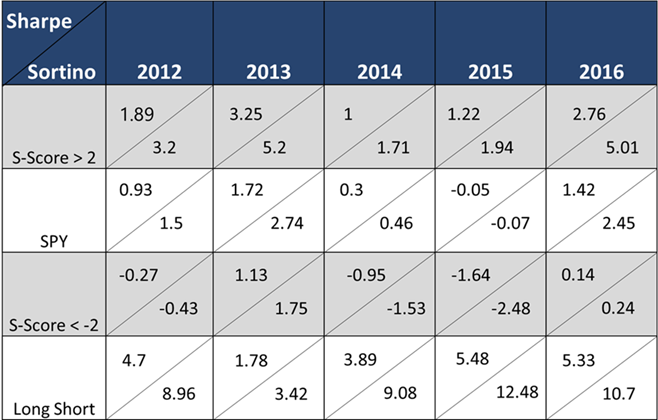

Last year was a good year for SMA data. High sentiment securities outperformed and low sentiment securities underperformed with good Sharpe’s and Sortino’s. The below tables contain returns and Sharpe/Sortino ratios for the full history of Social Market Analytics S-Factor data. Correlations to standard factors continue to be near zero. I’m sure our data can help in your investment process, contact us to learn more.

Five-year return summary:

Sharpe / Sortino

Leave a Reply

Want to join the discussion?Feel free to contribute!